-

BOJ rate hike and the reduction in Bond buying program came as expected. The 0.25% hike was the highest since 2008, which was a large surprise to us.

-

While the Bond buying program only scaled back by half, from 6 trillion Yen to 3 trillion Yen.

-

The decision to hike to 0.25% is mainly attributed to improvement in inflationary pressure and the Japanese Government’s ability to keep the 2% pace of inflation in check.

-

All eyes will be on Powell tonight for the FOMC and the dovish tone will send the Yen into higher grounds.

Rate hike and tapering of bond purchase in line with expectation, but surprise on the aggressive hike to 0.25%

The Bank of Japan’s commitment to hike its rate and reduce its bond buying program is in-line with our expectation, highlighted in our previous report dated 29 Jul 24 (Read here for more information). We believe that the BOJ rate hike is attributed to the following factors and may affect future rate increases should the needle move:

- Japan’s inflationary pressure has been declining and reached 2.8% in the latest reading. This gives the BOJ a huge boost of confidence to initiate a rate hike.

- The BOJ believes that with the current pace of inflationary pressure, they are able to achieve and maintain a 2% rate. We believe this will be a challenge as inflationary pressure is partly attributed to external factors such as a weak yen and energy import prices. Internal consumption remains low despite an improvement in retail sales, which stand at 3.3%.

- The Bank of Japan is looking at a highly anticipated rate cut in September, which explains the bold move by the BOJ to increase the rate aggressively.

- The rate hike may give additional support to its currency intervention should the yen weaken further.

However, the commitment to reduce its bond purchases sparks a lack of confidence in the Bank of Japan, as the reduction is only halved, from 6 trillion yen to 3 trillion yen.

Key risk of BOJ policy: Fed’s non commitment to hike rate and continued weakness in Yen due to carry trade

The FOMC meeting tonight (July 31, 2024) will likely be a non-event, but the possible dovish tone may help the yen to prop up. However, there exists a slight possibility of an actual non-event, and should this happen, the yen will likely weaken further. The weakness of the yen will be crucial, as it has yet to recover to the lows of 140.50 seen back in December 2023.

Carry trade between the US dollar and Japanese yen will likely continue as usual. The 3-month and 6-month USDJPY forward rates stand at 150.70 and 150.67, respectively.

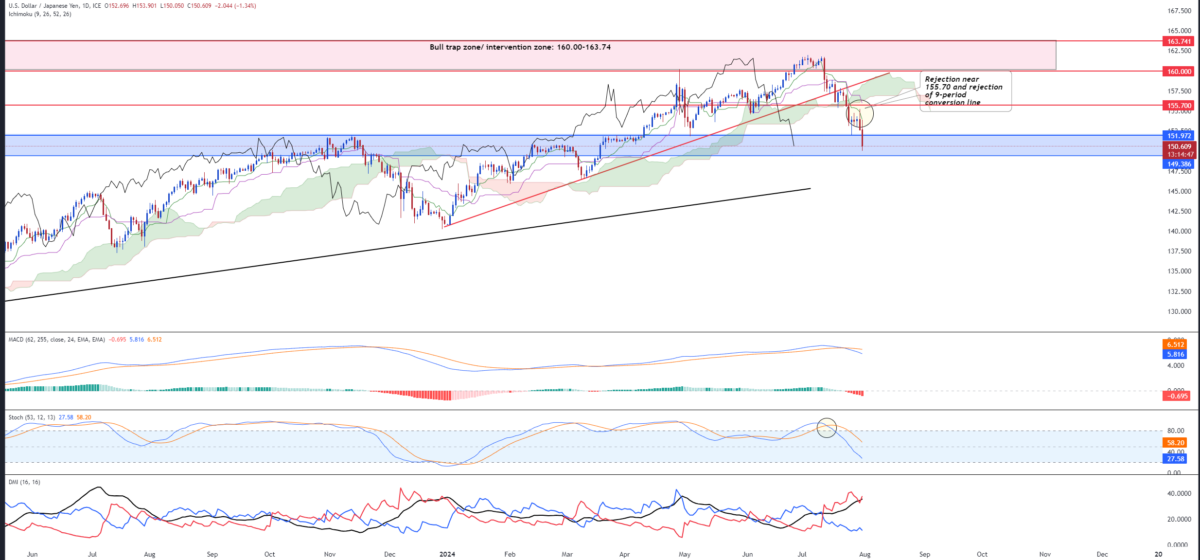

Technical outlook on USDJPY – In a bearish trend, nearing 149.38 target support

The Japanese Yen continued lower after a brief and weak rebound above 151.97 based on our previous technical outlook on 29 Jul 24 (Read here for more information). The consolidation in the short-term is forgo but we got it on point to sell on rebound after adverse rejection near 155.70 on Tuesday 30 Jul 24. We maintain our bearish outlook for USDJPY and maintain our TP at 149.38. Below are the key pointers:

- Ichimoku has formed the three bearish death cross in sequence.

- Long-term MACD is showing a clear bearish signal over the longer-term period as the histogram has turned negative. The MACD/Signal line has performed a crossover at the top

- The stochastic oscillator has confirmed the overbought crossover.

- Bearish momentum is strong and though a rebound at 149.38 is possible, the strength of the rebound will be crucial in the future.

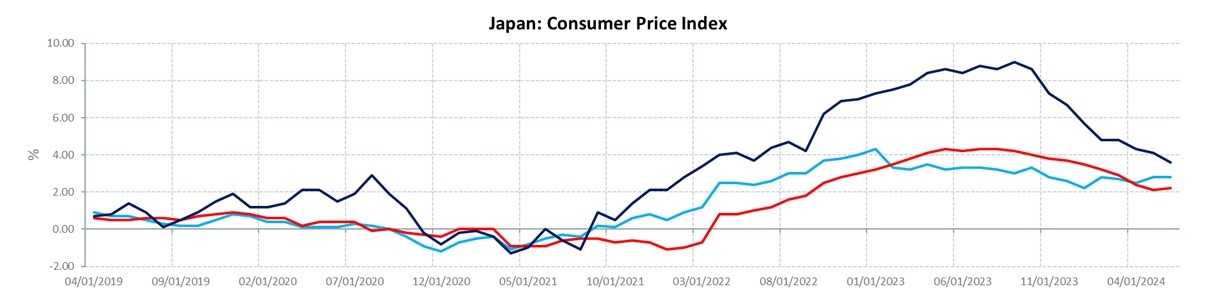

Figure 1: Japan CPI – nearing 2% target

Red: Core CPI, Blue: Headline CPI , Black: Food inflation

Sources: CGSI RESEARCH, CEIC

Please refer to the disclaimer here.