- October 2024 marked a strong loan growth for Singapore’s banking system.

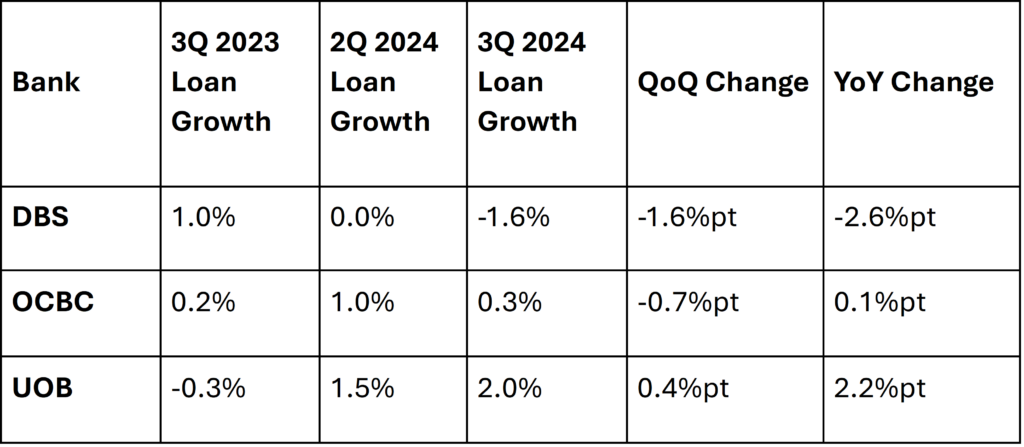

- UOB showed the most robust loan growth in 3Q 2024, with positive quarter-on-quarter and year-on-year changes.

- For the 2025 loan growth target, UOB has projected high single-digit growth, while DBS estimates 4-5% growth.

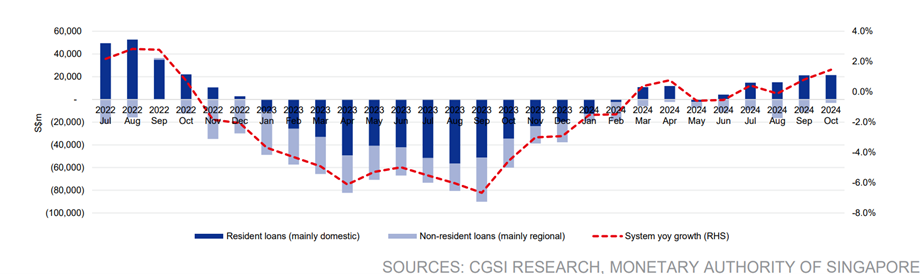

In October 2024, Singapore’s banking system experienced a 1.5% year-on-year (YoY) loan growth, primarily driven by domestic loans. This growth marks a significant improvement compared to the flat growth observed from January to September 2024, likely spurred by positive investment sentiment following a 50 basis points interest rate cut by the US Federal Reserve in September 2024.

Singapore’s banking sector is a cornerstone of the Singapore Exchange (SGX) market. The three major banks in Singapore—DBS Group Holdings Ltd (SGX:D05), Oversea-Chinese Banking Corporation Ltd (OCBC) (SGX:O39), and United Overseas Bank Ltd (UOB) (SGX:U11) —are key components of the Straits Times Index (STI), which tracks the top 30 companies on the SGX.

Banking System Loan Growth Gaining Momentum

Comparison of Loan Growth Among DBS, OCBC, and UOB

Source: CGSI Research

Following the overview of loan growth, let’s delve into the performance of each bank in 3Q 2024, their strategic steps, asset quality, and loan growth targets:

3Q 2024 Performance

DBS: DBS saw increases in trade loans, non-trade corporate loans, and consumer loans. However, the bank faced loan growth challenges in the Hong Kong market, impacted by China’s economic conditions.

OCBC: OCBC’s loan growth was driven by corporate loans, mortgages, and sustainable financing. Geographically, Singapore, Malaysia, the UK, and Australia were key contributors. Corporate, SME, and consumer/private banking account for 56%, 9%, and 35% of the loan book, respectively.

UOB: UOB’s loan growth was supported by wholesale trade loans and retail mortgages. ASEAN’s role as a trade hub, the rise of the digital economy, and the growth of the green economy boosted its loan books.

Strategic Steps

DBS: DBS has been conservative in its approach to the Hong Kong market and the real estate market, decreasing its SME loan book in the past years and focusing on large, blue-chip players in real estate.

OCBC: Regarding OCBC’s China exposure, the bank lends to Chinese companies operating outside China, particularly in ASEAN. Besides that, the bank’s sustainable financing loans rose significantly, 31% YoY in 3Q 2024 to S$47.1 billion, comprising 15% of its total customer loans.

UOB: Capital management was a key focus in 3Q24’s earnings briefing, UOB has excess capital of S$2.5 billion available for shareholder return. UOB’s capital plans will be announced in early 2025. The bank has not detected any significant stresses in its loan portfolio thus far. Areas of loan growth include ASEAN from the “China +1” strategy and Johor data centres, which have already attracted 17 new direct investments to the Johor Bahru Special Economic Zone (JB SEZ).

Asset Quality

DBS: DBS maintained resilient asset quality, with the non-performing loan (NPL) ratio falling to 1.0%. The bank reported a decline in non-performing assets due to repayments, upgrades, and write-offs. Specific allowances remained below the cycle average, reflecting strong asset quality management.

OCBC: OCBC’s asset quality remained strong, with an NPL ratio of 0.9%. The bank has elevated net new non-performing assets from downgraded real estate exposure in Hong Kong, these were largely secured and did not require substantial provisions.

UOB: UOB’s asset quality remained stable, with an NPL ratio of 1.5%. The bank maintained prudent levels of general allowances on loans, with performing loans coverage at 0.9%. The hefty specific provisions in 3Q24 were mainly due to the integration of its Citi retail portfolio in Thailand, which is expected to normalize in the next two quarters.

Loan Growth Target

DBS: The bank forecasts a 4-5% loan growth, seeing reasonably healthy pipelines across both geographies and sectors. With the Trump administration, DBS predicts more volatility in interest rates and FX. If rates go up, DBS expects to see loan growth a bit muted but tailwinds in net interest income.

OCBC: The bank has not released its FY2025 outlook but is firmly positioned to meet its 2024 targets, with OCBC aiming for low single-digit loan growth in FY2024. OCBC said the market in 2025 will be a bit more uncertain as to how loans will grow, with the interest rate expected to stay higher for longer.

UOB: UOB is projecting high single-digit loan growth for 2025, which is higher than its FY2024 low single-digit guidance.

Moving forward, investors should monitor updates on Fed monetary policy, announcements from the Monetary Authority of Singapore, and guidance from bank management teams on loan growth and other key metrics that can provide valuable insights.

Disclaimer: ProsperUs Manager of Content, Hailey Chung, does not own shares of the company.