It was the turn of one of the biggest electric vehicle (EV) makers to post its earnings.

EV maker Tesla Inc (NASDAQ: TSLA) posted another record-breaking quarter in Q4 FY2022.

Revenue jumped by 37.2% year-on-year (yoy) to US$24.3 billion, beating market expectations of US$24.1 billion.

Tesla’s adjusted earnings also beat Wall Street’s expectations of US$1.12 earnings per share (EPS) and came in at US$1.19 EPS.

The strong performance was well-received by investors as Tesla’s share price rallied by about 5% in after-hours trading.

Looking at the latest financial numbers and its earnings call with analysts, here are five key takeaways for investors who are interested in investing in the EV giant.

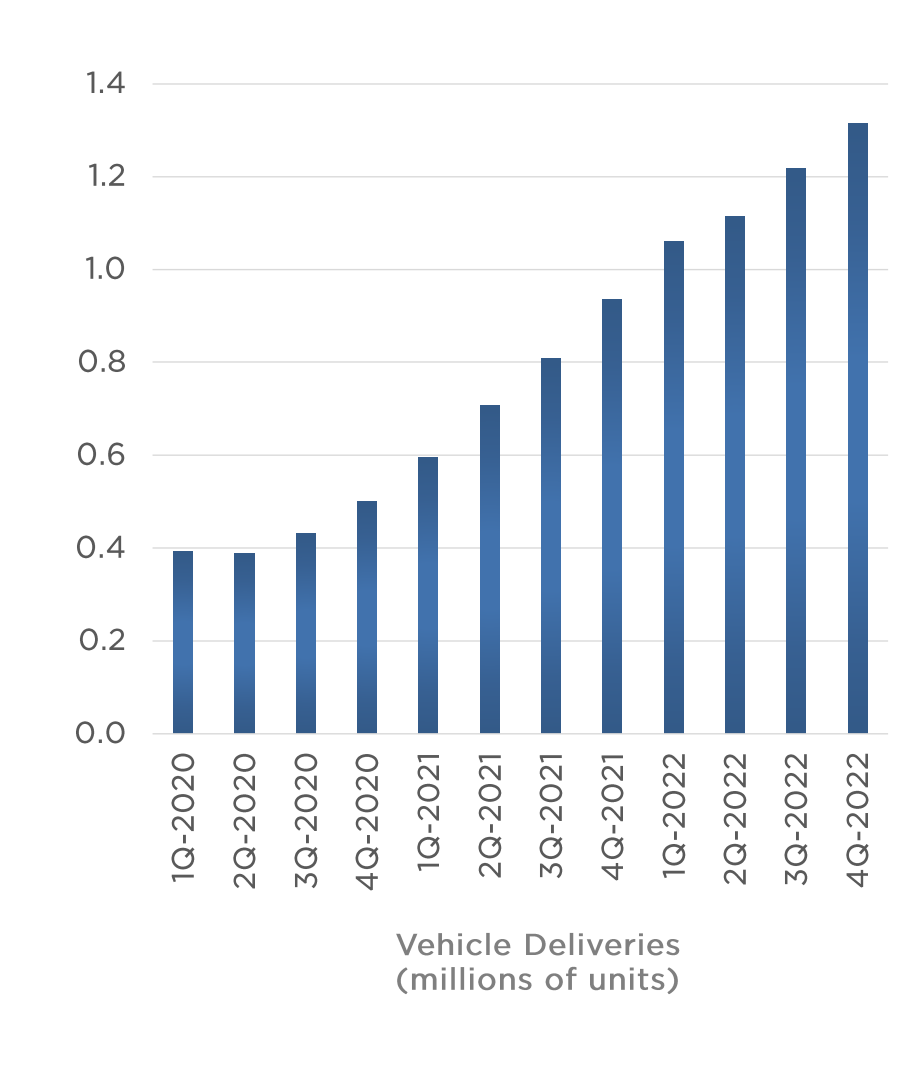

1. Strong vehicle deliveries despite challenging environment

Tesla posted record deliveries of over 1.3 million cars in 2022 despite the challenging environment, involving the forced shutdowns of some of its factories.

In Q4 FY2022, Tesla produced 439,701 vehicles and delivered 405,278 vehicles, which represents year-on-year (yoy) growth of 44% and 31% respectively.

For the full year FY2022, total production and deliveries jumped by 47% yoy and 40% yoy to 1.37 million and 1.31 million vehicles respectively.

Source: Tesla’s Q4 and FY2022 Update (Key Metrics: Trailing 12-Months)

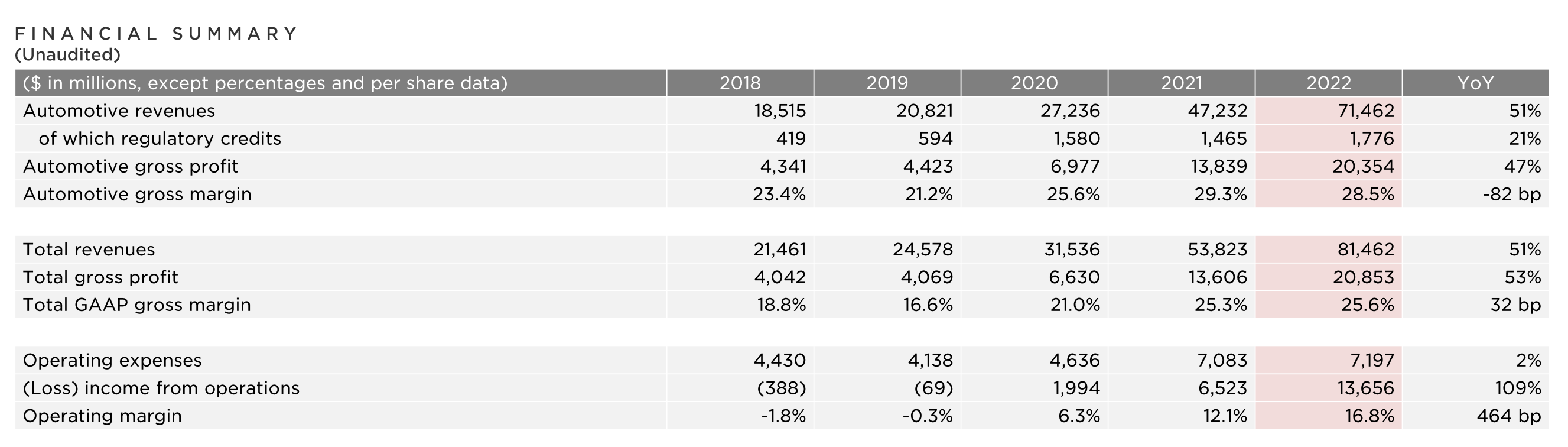

2. Automotive gross margin moderates

Tesla’s automotive gross margin moderated to 28.5% in FY2022 as compared to 29.3% a year ago.

During Q4 FY2022, automotive gross margin fell to a two-year low of 25.9%.

The decline in margin was mainly due to higher raw material costs and a negative foreign exchange (FX) impact.

It will be interesting to see how the margin will be affected following the number of price cuts that were introduced in various markets including the US, China (for the second time) and some European markets.

Those cuts did not happen until the beginning of this year so those effects are not reflected in Q4 FY2022 earnings.

Tesla’s CFO, Zack Kirkhorn, said on the earnings call that Tesla expects to maintain 20% automotive gross margins despite recent price cuts.

This would still be a considerable step-down from its current automotive gross margin level.

Source: Tesla’s Q4 and FY2022 Update

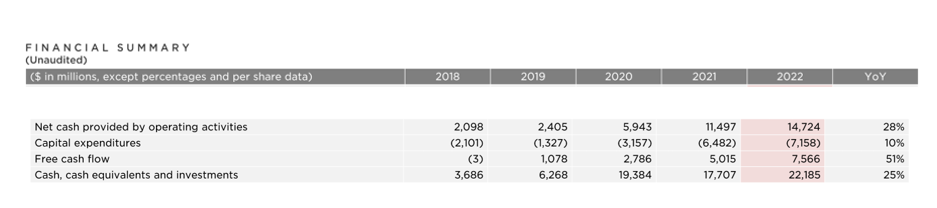

3. Strong cash position to withstand a potential recession

In FY2022, Tesla generated US$7.57 billion in free cash flow, bringing its cash and cash equivalent position to more than US$20 billion.

During the earnings call, Elon Musk, CEO of Tesla, said that Tesla’s strong cash position of more than US$20 billion will help Tesla get through a recession.

I feel we’re in a very strong position to get through a recession, because we really don’t have any debt. And we’ve got over $20 billion of cash, which is great. The cash is earning a ridiculous return, a good return. So it’s like nontrivial. And the interest rate actually in the $20 billion is earning like quite a good amount.

Source: Tesla’s Q4 and FY2022 Update

4. Ramp up production to 1.8 million vehicles in 2023

Tesla kept its long-term delivery target of 50% compounded annual growth rate (CAGR) despite falling off the pace in recent quarters amid the production disruptions.

For 2023, Tesla expects to remain ahead of its long-term 50% CAGR with around 1.8 million cars delivery target.

In fact, Musk shared that Tesla has the potential to do 2 million cars in 2023 but management remains cautious on any potential interruption to the supply chain.

However, production for Cybertruck, its new electric pickup truck, would not begin volume production until next year.

5. Demand for Tesla is double that of the production rate

Tesla’s aggressive price cuts at the beginning of this year has spurred a wave of demand for its EVs.

While this has positioned Tesla as the initiator of a price war in the industry, it has propelled buyers to sit up and take notice.

In fact, Musk shared that orders in January were twice the rate of its production and that “these price changes really make a difference for the average consumer.”

The strong brand and margin that Tesla has gave it the room to cut prices and pressure its competition.

To put it into perspective, Tesla is one of the few EV makers that is profitable and its net profit per vehicle was more than seven times that of Toyota Motor, one of the largest automotive players in the world.

There is concern that cooling demand, coupled with its price cuts, could hurt Tesla more than management expected but Musk appears bullish that demand will remain strong for Tesla EVs.

Tesla’s valuation is much more reasonable now

One of my main concerns on Tesla has always been valuation but following a decline of more than 50% over the last year, I believe that investors will find it to be a more reasonable entry point at this level.

In April last year, I shared about Tesla’s impressive earnings but highlighted its share price as expensive.

At that time, Tesla was trading at a forward price-earnings (PE) of more than 100x and a trailing PE of 200x.

Today, it is trading at a forward PE of 40x and trailing PE of 44.4x. Those are much more attractive levels for long-term investors.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.