In Singapore, we are still in the midst of REITs’ earnings and business updates for the latest periods. So far, most large REITs have recorded relatively solid numbers despite a challenging environment.

That “environment” is high interest rates in the US and above-average worldwide inflation.

Yet as we move into 2023, the picture might be brighter for REITs.

One popular REIT which has unique Europe exposure – and is also a constituent member of the Straits Times Index – is logistics-focused REIT Frasers Logistics & Commercial Trust (SGX: BUOU).

Last week, it announced its latest Q1 FY2023 business update (for the three months ending 31 December 2022).

So, how did the REIT perform and is it worth a second look for dividend investors looking to get back into the Singapore stock market?

Encouraging rental reversions during the quarter

One of the biggest things for REITs in this higher interest rate environment is the ability to raise rents at or above the cost of funding.

On this front, Frasers Logistics & Commercial Trust (also known as FLCT) did relatively well.

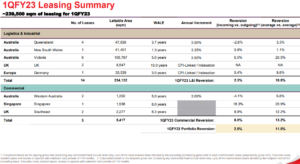

During the quarter, the REIT saw average rental reversions come in at a robust positive rate of +11.0%.

However, it was its commercial properties – which only make up 30% or so of its overall portfolio value of S$6.7 billion – where its reversions came in strongest.

In Singapore, a lease at Alexandra Technopark saw a strong positive rental reversion of +20.9%, boosting its overall commercial rental reversion rate to a positive +13.2% for the period (see below).

Source: Frasers Logistics & Commercial Trust Q1 FY2023 business update slides

All this was a surprise given FLCT’s commercial portfolio’s occupancy rate (89.8%) actually dragged down the overall portfolio occupancy rate to 95.9% for the period (from 96.5% as of the end of September 2022).

This came from weakness in two Australian business parks, which saw lower occupancies during the period.

Meanwhile, its logistics and industrial (L&I) portfolio remained its rock-solid 100% portfolio occupancy.

Overall, the REIT managed to reduce FY2023 expiries to 4.7% of gross rental income (GRI) from the previous 10% as of the end of September 2022.

Capital management position remains flexible

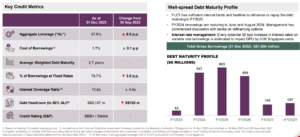

On the capital management side of things, FLCT has maintained its robust position and metrics.

Its gearing ratio, at just 27.9%, is one of the lowest for a large-cap Singapore REIT – giving it debt headroom of just over S$3 billion before it hits the 50% MAS-imposed gearing limit.

On the cost of borrowings, this also looked attractive at just 1.7% as of 31 December 2022, up only 10 basis points (bps) over the three months (see below).

Source: Frasers Logistics & Commercial Trust Q1 FY2023 business update slides

Management did guide that this could rise to 2-2.5% by the end of FY2023. But even if it did, that’s still a reasonable borrowing cost in the current environment.

Management also said that for every 50 bps increase in interest rates, its distribution per unit (DPU) would be negatively impacted by 0.06 Singapore cents.

Based on its latest H2 FY2022 DPU of 3.77 Singapore cents, that would be a 1.5% decline in FLCT’s half-year dividend.

One thing to watch is the REIT’s debt maturity profile, with over half of its total debt load coming due in FY2024 and FY2025.

Yielding over 5.5% for dividend investors

Overall, it wasn’t a quarter that was any surprise for FLCT shareholders. It was positive on the rental reversion rates, showing that perhaps the economic picture isn’t so dire globally just yet.

It’s a unique REIT that has sizeable exposure to Europe but REIT invetsors should note that just over 50% of FLCT’s portfolio (by value) is held with Australian properties.

That means that while there is some upside exposure to Europe, it might not be as much as investors first think.

With a 12-month forward distribution yield of 5.6%, FLCT shares are up nearly 30% off their 52-week low.

This could provide an opportunity for income investors who are bullish on logistics and industrial properties in Europe and Australia over the next decade.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips doesn’t own shares of any companies mentioned.