In this era of seemingly ever-rising interest rates, many Singapore REIT investors have been focused on gearing ratios.

Ideally, you’ll want a low gearing ratio and, as I’ve written about previously, China-focused outlet mall operator Sasseur REIT (SGX: CRPU) has one of the lowest gearing ratios among all Singapore REITs.

Sasseur REIT also happened to report its Q1 2023 business update on Wednesday (10 May) before the Singapore stock market opened.

So, for S-REIT investors bullish on the China reopening story, here’s all you need to know on Sasseur REIT’s latest Q1 2023 earnings.

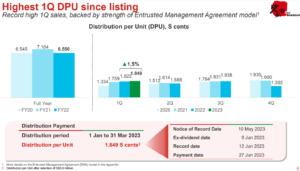

Sasseur REIT’s DPU a record high for Q1

The REIT, which owns four premium outlet malls in China, recorded a distribution per unit (DPU) of 1.849 Singapore cents for Q1 2023.

This was up 1.5% year-on-year and was also the highest Q1 payout for Sasseur REIT since listing on the Singapore Exchange (SGX) in 2018 (see below).

Source: Sasseur REIT Q1 2023 business and operational update

Driving this was a 3.8% retention, or S$900k, of distributable income for working capital purposes.

Management also pointed to the strength of its entrusted management agreement model (EMA) during the period, with total outlet sales for its portfolio up 17.9% year-on-year to RMB 1.29 billion (S$247 million).

With part of its business model derived from pegging a portion of rents to tenant sales, this better aligns the interests of the mall owner, tenants and REIT’s unitholders.

Meanwhile, overall EMA rental income (including the fixed component) rose 7.7% year-on-year to RMB 170.6 million for Q1 2023.

In some positive news on the reopening, Sasseur REIT announced that its Hefei outlet’s sales during the period were higher than the pre-Covid Q1 2019 quarter.

Meanwhile, its Chongqing Liangjiang outlet recorded its highest-ever quarterly sales.

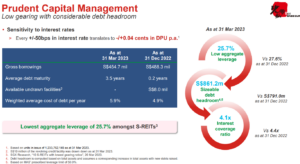

Robust balance sheet and lower gearing ratio

Sasseur REIT recorded an even lower gearing ratio of 25.7% as of 31 March 2023, down from the 27.6% as of 31 December 2022.

In addition, its average debt maturity has been significantly extended to 3.5 years (from just 0.2 years as of 31 December 2022) although that has come with a rise in its weighted average cost of debt to 5.9% (see below).

Source: Sasseur REIT Q1 2023 business and operational update

Its interest coverage ratio (ICR) remains solid at 4.4 times while management did also state the REIT’s sensitivity to interest rates in that every 50 basis point (bp) rise in rates would means 0.04 Singapore cent cut in DPU.

Portfolio occupancy rises and proactive efforts on 2023 leases

For Sasseur REIT, its portfolio occupancy rate of 96.6% in Q1 2023 was up from 95.4% in Q1 2022. However, it was down sequentially from 97.2% in Q4 2022.

This was mainly down to its Kunming mall, where the REIT had to make trade mix adjustments to replace weaker tenants impacted by the fall in domestic travel in the region.

On the weighed average lease expiry (WALE) side, Sasseur REIT has reduced the proportion of leases expiring in 2023 from 52.7% to 47.7% (by NLA) during Q1 2023.

Management stated that there have been deliberately short leases to optimise tenant mix and accommodate pop-up stores in Q1 2023 as the REIT adapts to the fast-changing consumer scene in China.

Solid yield and a quarterly dividend payer

It was a positive quarter for Sasseur REIT as it looks to rebound from a turbulent few years during which China had periodic lockdowns due to Covid-19.

Management did say that the outlet mall industry is growing fast and, as many investors are asking, it will look to acquisitions to grow its asset base.

The REIT’s management will first look to Xi’an and Guiyang as its sponsor has two outlet malls there which Sasseur REIT has Right of First Refusal (ROFR) on.

As one of the few S-REITs that pays a quarterly dividend, Sasseur REIT’s shares are now providing a dividend yield of 9.7% on a 12-month forward basis.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips doesn’t own shares of any companies mentioned.