Investment Ideas for the Great Transition

October 20, 2021

The US Federal Reserve has signalled the imminent start of the transition from the Great Stimulus of 2020-2021 to a period with new uncertainties.

The “bad news is good news” paradigm of the COVID-19 pandemic is likely over. This was when disease and economic decline was good news for financial markets because they meant continuation of the greatest monetary and fiscal stimulus since the Second World War.

In its place, we expect to see the gradual withdrawal of stimulus, slowing economic and earnings growth, and higher inflation.

This will likely slow US equities returns to a crawl. Indeed, higher rates and yields are generally not good for Emerging Markets either.

So, investors have to be very selective – in both sectors and specific stocks.

And it will likely pressure downward the value of US Treasury paper, and likewise edge down US corporate credits, albeit with a lag.

The US Dollar could then stage a rebound in response to higher yields.

The Fed signals November taper

Unless there is a significant change in economic circumstances, we will get tapering from November this year, at US$15 billion a month, to complete by June next year.

This has been clearly signalled by the Federal Reserve (Fed). And this is at the hawkish end of the range of expectations.

The message from the US Treasury market is that inflation is running hot and cheap money is running out of time.

In late September, the 10-year US Treasury yield broke out of an “ascending triangle pattern” (formed from mid-August to late-September), rising fairly quickly from 1.3% to a recent high of 1.63%, before easing to 1.57%.

Our sense is that with tapering now almost upon us and inflation a clear and present problem, the 10Y UST yield will push higher over coming months.

And this is a problem for equities because valuations are inverse to the discount rate.

Inflation likely to be with us longer than expected

The Fed has gone a bit quiet on that expression “it’s transitory”. The latest data for US headline inflation hit 5.4% for the 12 months to September.

Core inflation for the same period was 4%. All of this is way above the Fed’s average inflation target of 2%. Energy prices – from coal to natural gas to crude oil – have gone through the proverbial roof.

Meanwhile, supply chains remain badly disrupted by the pandemic. And all of that is showing up in a relentless surge in producer price inflation around the world.

The “VILE Economy” Redux?

The Global Financial Crisis term “VILE Economy” – “volatile inflation, less expansionary economy” – has made a comeback in recent months.

So, here’s our take on the “VILE Economy” 2022. The spread of the Delta variant has smashed hopes for a neat exit from the COVID-19 pandemic. It will now likely be a messy, desynchronised, 2-steps forward, 1-step back process.

Even highly-vaccinated societies are finding reopening fraught with surges in cases, threatening to overwhelm hospitals.

So, we could find ourselves in a stop-start process of reopening around the world, as governments are forced to constantly calibrate the pace of reopening with an eye on available hospital beds.

The slow vaccination of the Emerging Markets ex-China will add to the mess – worsening that desynchronised return to normality in different countries.

Economically, that means we are likely to see slowing economic growth beyond the “pop” that we saw earlier this year.

Implications for interest rates

Note that the median view of the Fed’s FOMC (Federal Open Market Committee) members regarding the appropriate Fed Funds Rate for 2022 has lifted from 0.1% at the June FOMC meeting to 0.3% recently.

That means the median view of the FOMC members is the rates lift-off should happen next year.

And the market is viewing the pace of the taper as clearing the decks for a rates lift-off in the second half of next year.

That ticking clock – counting down the months before the rates lift-off – is not going to be helpful for equities.

US equities: expect low returns from here

Our sense is that we will either see small gains in the coming months or indeed a correction in the face of the likely peaks in economic growth, earnings growth and policy stimulus.

Given that tech stocks have a larger part of their valuations in more distant earnings, they will suffer more “duration risk” than stocks in the more “traditional sectors”.

And so, we would also expect growth stocks to do worse in coming months than value stocks as peak stimulus gives way to the taper.

Seek out opportunities in select areas

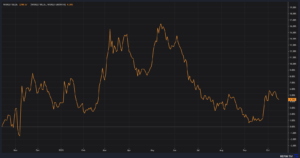

The MSCI World Value Index has started to outperform the MSCI Growth Index very recently (see below).

Source: Refinitiv

So, you’re looking at financials, health care, consumer staples, among other sectors within that broad “investment style”.

Banks are more defensive than tech stocks – which dominate the MSCI World Growth Index – in a rising interest rate environment because of the likelihood of rising net interest margins.

Energy stocks, to be clear, have rallied big time. The S&P 500 energy sector index is up 152% from its March 2020 low.

So, we are probably in the second half of the game, as it were, maybe even the final quarter. But with supplies of coal and natural gas unable to cope with demand – and OPEC-Plus holding back crude oil supply – we could see yet higher prices as we approach the northern winter.

The strengthening of the US Dollar in response to higher US Treasury yields (driving the USD/JPY from 109 to 114 in less than a month) could support Japanese equities in coming months.

There is often a positive correlation between the USD/JPY and the Nikkei, and the logic is a weak Yen is a boon for Japanese exporters’ earnings in local currency terms.

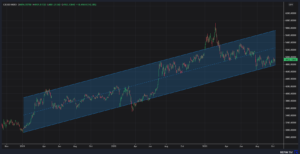

Chinese equities are out of favour and beaten down. But the CSI 300 has seen some tentative support at the bottom of an uptrend channel from 2009 (see below).

Source: Refinitiv

The doomsayers on China have been at it – and wrong – since 2001 when Gordon Chang published his then much-cited book “The Coming Collapse of China”.

There have been countless similar unfulfilled prophesies of China’s doom over the 20 years since.

Indeed, the current crisis in the Chinese property sector is likely to prompt policy makers to ease monetary conditions to stabilise the economy.

This could present a bargain-hunting opportunity for Chinese stocks and China-related plays in the Singapore market.

Say Boon Lim

Say Boon Lim is CGS-CIMB's Melbourne-based Chief Investment Strategist. Over his 40-year career, he has worked in financial media, and banking and finance. Among other things, he has served as Chief Investment Officer for DBS Bank and Chief Investment Strategist for Standard Chartered Bank.

Say Boon has two passions - markets and martial arts. He has trained in Wing Chun Kung Fu and holds black belts in Shitoryu Karate and Shukokai Karate. Oh, and he loves a beer!