ESG Investing in Asia: What Should Investors Buy?

September 13, 2021

Globally, the Covid-19 pandemic was widely-recognised as a watershed moment for all things environmental, social and governance (ESG).

Take power generation and the key role it will play given its impact on climate change.

In the US in 2020, according to the US Energy Information Administration (EIA), renewables became the second-most prevalent source of electricity.

Renewables actually overtook coal (21% vs. 19% of the energy mix) for the first time and it was telling that it was the only US electricity source to actually expand in 2020.

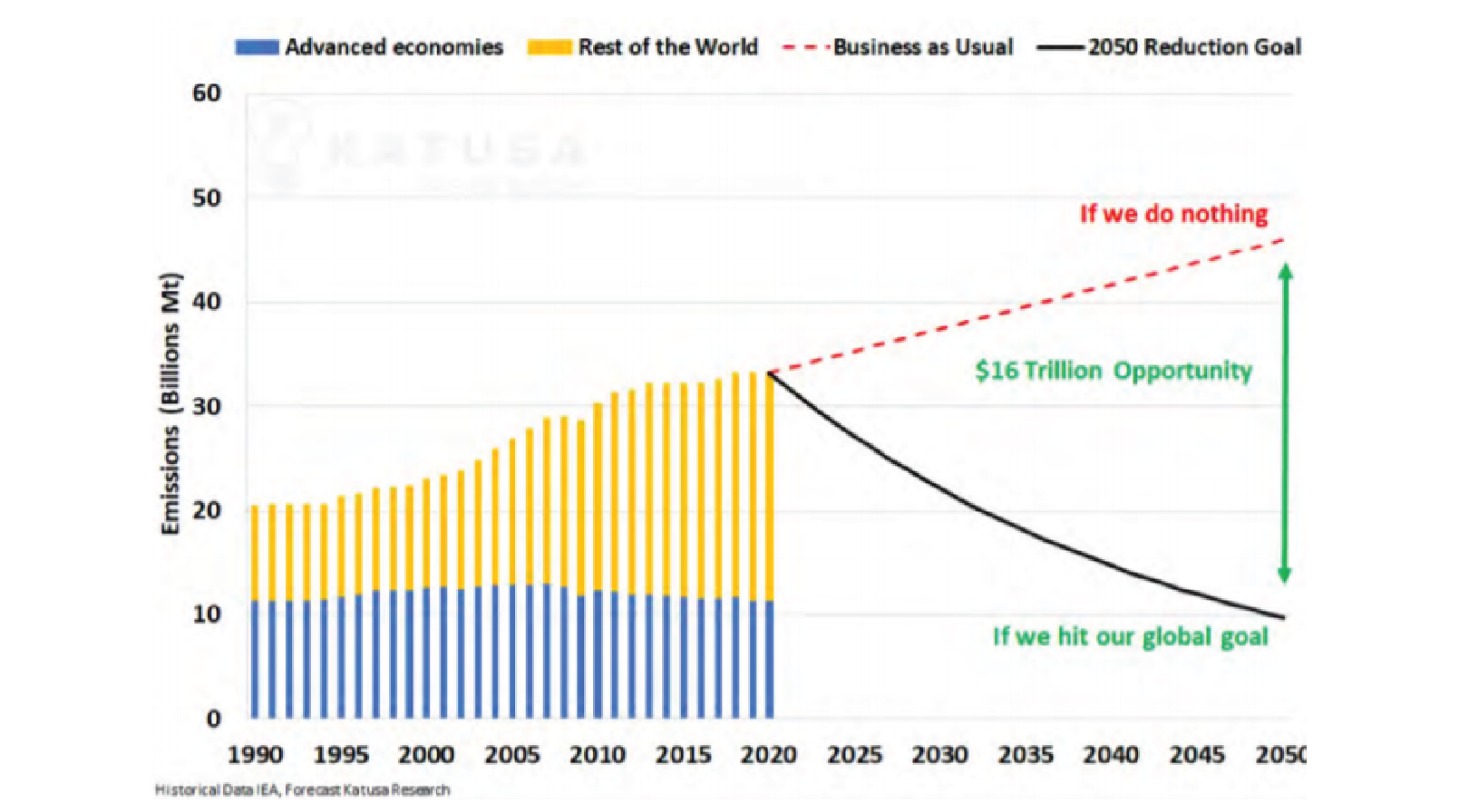

Advanced economies have gradually been able to reduce their CO₂ emissions in recent years. In a 2020 report from the International Energy Agency (IEA), advanced economies in fact saw 2019 CO₂ emissions fall by 3.2% on 2018 levels even as CO₂ emissions in the “Rest of the World” increased.

In the process, that’s creating an enormous US$16 trillion opportunity to de-carbonise the planet by 2050 – most of the future “work on the ground” will have to come from outside advanced economies (see Figure 1 below).

Figure 1: Global energy- related CO2 emissions

Therein lies a lesson for investors in Asia. The opportunity set that is set to come out of Asia in the ESG space, ranging from climate change to corporate governance and gender equality, is eye-opening in terms of its sheer scale.

Beating a different path

For long-term investors, it will be crucial to discern between how ESG and climate change mitigation measures grow and evolve in Asia versus how they have so far developed in the West.

Whereas the private sector had a crucial bottom-up role to play in both the US and Europe, with local and national governments being much more reactive in their ESG policy framework, Asia will likely see a more top-down approach.

This is no more clear than in China. In the world’s second-largest economy, and Asia’s largest, a national carbon trading exchange kicked off in the middle of 2021.

Setting a price on carbon is one of the first real steps towards reducing the carbon emissions of a broader economy.

A top-down approach from the national government in China played a part in this coming to fruition, where Beijing has set a date of 2060 for the Chinese economy to reach “carbon-neutrality”, or net-zero emissions.

Meanwhile, in one of the other big Asian economies, India is a country which will have an outsized impact on global energy use given it’s estimated to account for a whopping 25% of the rise in global energy use by 2040.

As a result, the Indian government is looking at ways of drastically reducing carbon emissions. One of the key ways to bring down its carbon footprint is by supporting emerging technologies.

In this regard, India is pushing ahead with schemes aimed at doing exactly that. In its 2021 Union Budget, the Indian government unveiled a plan to launch a National Hydrogen Mission that aims to collaborate in building an ecosystem for green hydrogen initiatives.

Plummeting costs

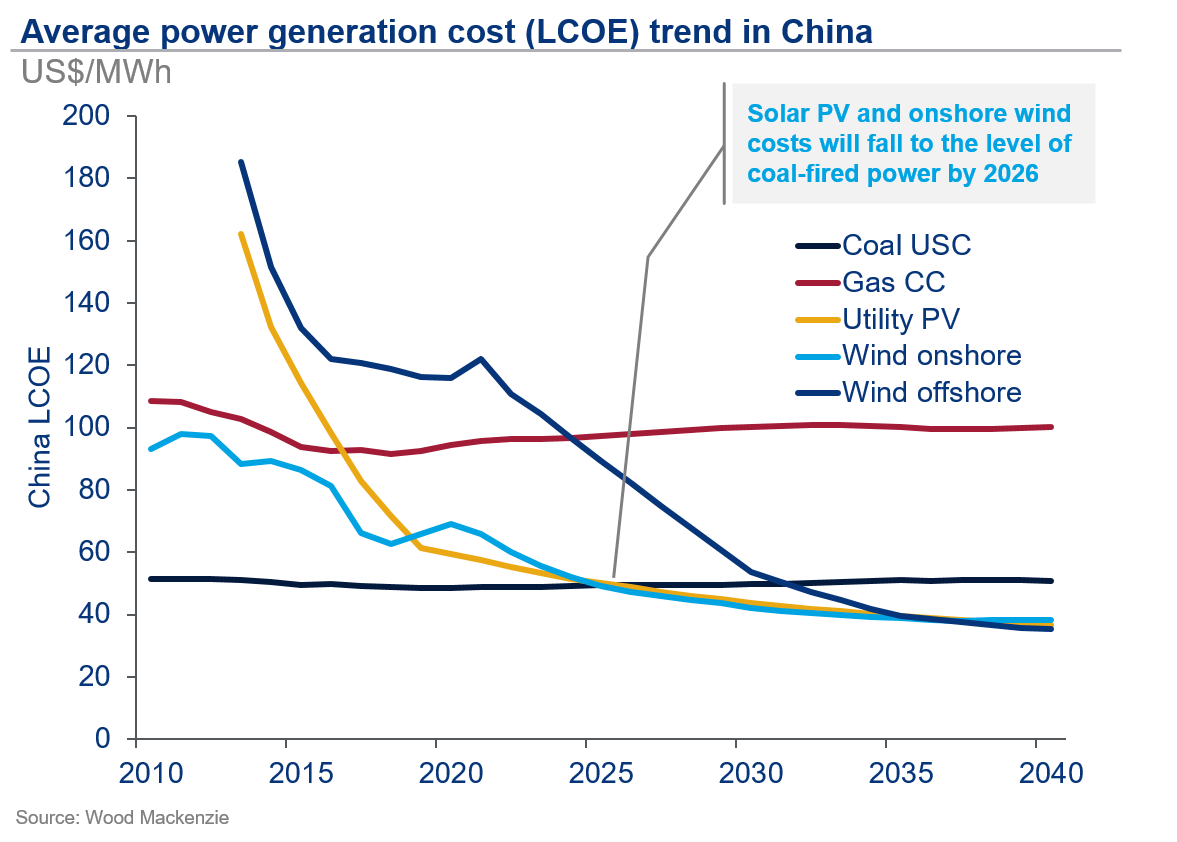

One of the big drivers of this structural shift has been the fall in costs for renewables more broadly. Also known as the levelized cost of electricity (LCOE), costs have fallen dramatically over the past decade.

In China, the most dramatic falls are being seen in photovoltaic (PV) solar and onshore wind, meaning they’ll likely be price-competitive by 2026, or perhaps even earlier (see Figure 2).

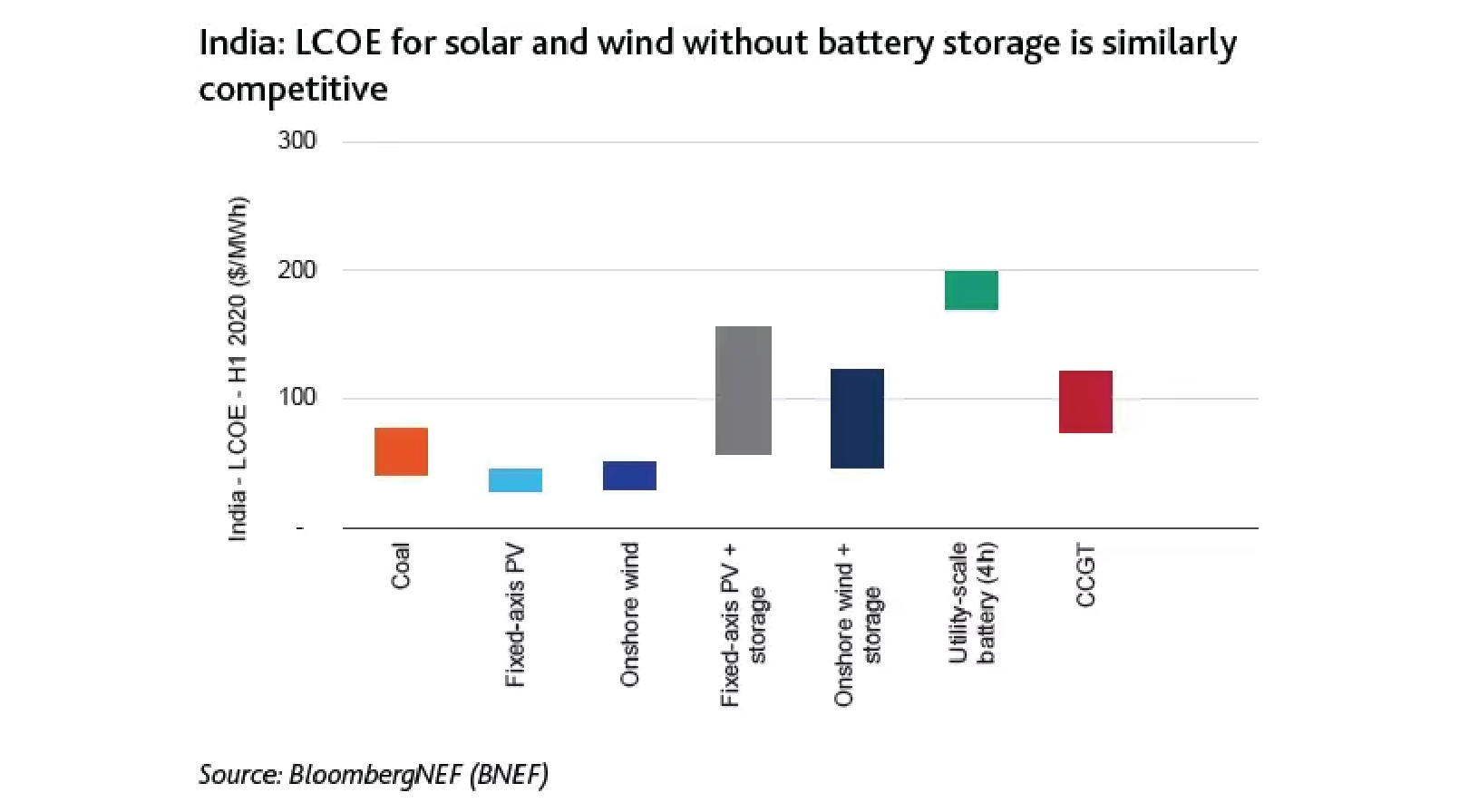

As for India, the country is already producing an LCOE for renewables that is beating out coal in certain situations (see Figure 3).

Figure 2: Average power generation cost (LCOE) trend in China

Figure 3: India’s LCOE across power sources for H1 2020

Across both markets, as in the West, one of the biggest challenges will be building out a nationwide battery storage system that can store and then distribute power when it’s needed (i.e., when the sun’s not shining and wind not blowing).

Wide opportunity set

So, for investors, what does this all mean for the long-term opportunity set in Asia? There’s no doubt that there will be a cornucopia of choice but it will take a clear-eyed investment framework and an on-the-ground team to identify the winners, as well as losers.

In regard to specific sectors, the scale and cost advantage of Chinese advanced solar PV manufacturers means some of the world’s leading producers of what will power the “net-zero” emissions goal are already residing in Asia.

The manufacturing of more energy-efficient wind power turbines also lends itself to the production heft and sophistication of supply chains evident in China.

Beyond that, though, there are smaller niche opportunities within the clean energy space. One great example is wind repowering projects, where older hardware on existing windfarms is replaced with updated and more modern equipment.

Much like improving current transport infrastructure, such as roads and bridges, rather than building a shiny new train line, wind repowering is an example of the type of opportunities investors will see during the massive infrastructure upgrades that are going to be needed in Asia, from China to Brazil.

The return on investment (ROI) in these projects can far outweigh what investors would typically receive on a new infrastructure project of a similar, or even bigger, scale.

More broadly, understanding which companies are committed to wider environmental goals, such as meeting a sub-set of the UN’s sustainable development goals (SDGs), will also be a barometer of how to measure whether management teams are serious about sustainability.

Extending beyond climate change

What’s even more pronounced is the fact that current Asian benchmark indices rarely take into account ESG-friendly policies when compiling which companies form key benchmarks.

That creates a real, and invaluable, opportunity for active investors to generate alpha by focusing on the overall sustainability of businesses. Why is that the case?

Because for most pension funds, endowments or institution-level investors, the ability to be sustainable is just as important (if not more so) than generating positive investment returns.

In fact, delivering robust investment returns while having a broadly positive impact on societies used to be viewed as mutually exclusive.

That assumption has been turned on its head as investors come to the realisation that sustainability can indeed be a key driver of investment returns.

Traditionally in Asia, “sustainability” or “ESG” has tended to focus on the “G” factor of corporate governance as relatively poorer standards of regulatory oversight meant that investors focused on identifying company management teams that were both ethical and which could maximise shareholder value.

It’s clear that that’s no longer enough when it comes to investing in Asia. While climate change and environmental factors will grow in importance, there will also be a new focus on the “social” aspects involved when generating returns.

Looking towards equality and inclusiveness

One big issue driving change in the social space is gender equality in terms of pay as well as board/senior management representation.

Women have traditionally been underrepresented at senior management and board levels. It hasn’t been a problem only found in Asia and has plagued many advanced economies too.

However, the data for having more women in these positions is resounding. According to Morgan Stanley in 2020, companies with high gender equity have outperformed low gender equity firms by an annualised 3.1% over the past eight years.

That’s just one of many examples but the trend is clear – companies that have more female representation at all levels tends to lead to relative outperformance in share prices.

The good news for investors in Asia is that many countries are already doing reasonably well when it comes to gender equity.

Perhaps the best, and biggest, example is China. China has a better record of having women be represented at senior management level than the rest of Asia-Pacific, according to a recent report from accounting firm Grant Thornton.

The study found that 95% of businesses in China employed at least one woman in senior management roles, compared to 83% for Asia-Pacific businesses and 87% globally.

Being selective is crucial

In this new environment for ESG investing, it will become clear that climate change will be a massive opportunity set when it comes to meeting the demand of a net-zero world.

However, that doesn’t mean that the only opportunities will emerge from the clean energy space.

Investors will have to adopt a comprehensive framework to analyse the overall ESG score that companies deserve based on a variety of factors, from gender diversity and carbon footprint to board structure and health & safety for employees.

One thing is clear for investors in Asia; the opportunity set will clearly be huge and the ability to leverage ESG when identifying winning stocks will become even more paramount to generating market-beating returns over the long term.

Tim Phillips

Tim, based in Singapore but from Hong Kong, caught the investing bug as a teenager and is a passionate advocate of responsible long-term investing as a great way to build wealth.

He has worked in various content roles at Schroders and the Motley Fool, with a focus on Asian stocks, but believes in buying great businesses – wherever they may be. He is also a certified SGX Academy Trainer.

In his spare time, Tim enjoys running after his two young sons, playing football and practicing yoga.