The recent violent sell-off in high-growth tech stocks in the US was a sign that higher interest rates are coming on the back of inflation that is clearly not “transitory”.

In that sense, it wasn’t a complete surprise. However, for those of us who are invested, or buying, growth stocks then the past few months have been painful to stomach.

Overall, though, these large sell-offs can create opportunities for investors to buy their favourite businesses at steeply-discounted prices.

Legendary investor Warren Buffett put it well when he says that:

“The most important quality for an investor is temperament, not intellect”.

So, holding on to great businesses for the long term should be our goal in these trying times. Beyond that, though, it’s also worth pondering what kind of stocks might perform well in this sort of inflationary environment.

Given how the word “inflation” probably came to define stock markets in 2021, higher prices aren’t necessarily bad for all sectors and businesses.

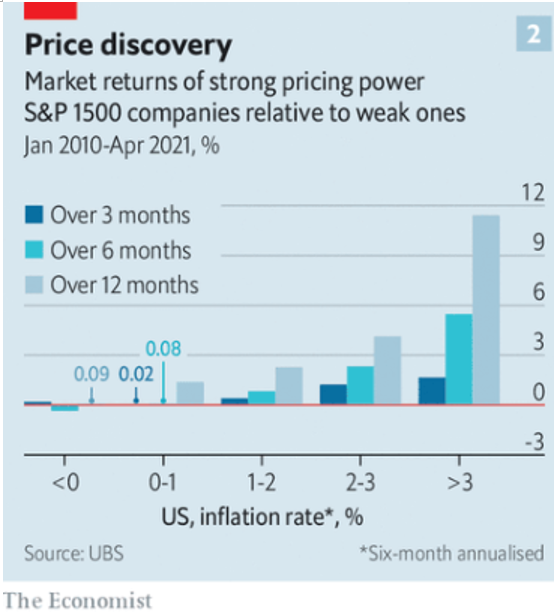

Look at pricing power

That’s because businesses in the US economy that can maintain “pricing power” (in effect the ability to raise prices without losing market share) should perform well when inflation is rising.

Naturally, we would think that energy companies and those with “real goods” built into their business would be better able to raise prices.

But actually, this is a mistake. Again, Warren Buffett put this succinctly when he said – in a 1983 Berkshire Hathaway (NYSE: BRK.B) shareholder newsletter – that:

“Any unleveraged business that requires some net tangible assets to operate (and almost all do) is hurt by inflation. Businesses needing little in the way of tangible assets simply are hurt the least”.

That was certainly true back in 1983 and, perhaps surprisingly, the same still holds true today. At least that’s what global bank UBS has found when constructing its “pricing-power score”.

In fact, companies that had strong pricing power, delivered better profit growth and also generated superior stock price returns during periods of higher inflation over the past 11 years or so (see below).

Understanding the sectors

So which sectors had the most pricing power? It was found that Consumer Staples, Communication Services and Information Technology have the most pricing power while Financials, Energy and Materials have the least.

In technology, understanding whether the business can command a higher price is key. After that, input costs should be relatively stable given a lot of the tech sector’s “value” is in intangible assets.

Perhaps that’s why there are concerns over tech companies that manufacture hardware, such as Apple Inc (NASDAQ: AAPL) and whether they’ll fare worse than other tech giants that don’t have to deal with supply chains and rising costs – like Alphabet Holdings Inc (NASDAQ: GOOGL).

For investors buying individual stocks during this period, understanding which technology firms (as many are also found in the Communication Services sector) can command higher prices will be the real challenge.

Scale will matter

When it does come to overall pricing power, even in times of relatively muted inflation, economies of scale kick in.

That means, at least in the retail sector, bigger businesses should have the ability to eventually pass on price increases to their customers.

In technology, the same scenario is perhaps less relevant as the advent of cloud computing and Software-as-a-Service has levelled the playing field for a lot of companies in terms of scalability.

Overall, investors looking at the next six months to a year should be focused on how companies in their portfolio can successfully navigate a period of higher inflation.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips doesn’t own shares of any companies mentioned.