-

Job data came in stronger than expected and with a potential uptick in Inflation which may inflict further rise in the 10-year yield to near 5%. This scenario may strengthen the dollar going forward as this may strengthen the resolve of the Fed to hold on to their rate cut in 2025.

-

Bank of Japan’s decision to raise rate may be hampered to a 50/50 chance despite a wage growth and rise in inflation. The reason being that the US commitment to cut the interest rate has cause the Japanese to be wary.

-

THE UK’s Gilts suffered another major blow after it rose sharply above the 4% mark. The sterling fell against the dollar as expected and has reached way beyond our target of 1.2680.

US Jobs Data Signals Fed Likely to Hold Rates in January. Surprise in CPI may add fuel to fire

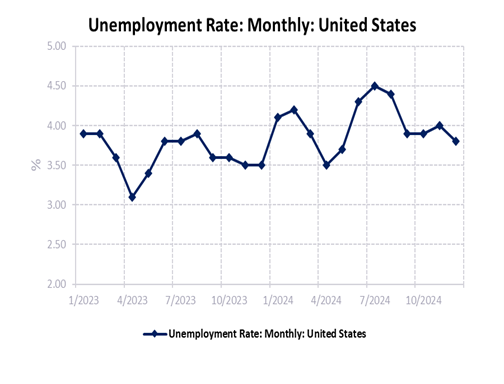

The latest US jobs report reveals a stronger-than-expected payroll increase of 256,000 in December, surpassing the consensus estimate of 165,000. Revisions to the previous two months showed a slight decline of 8,000. Meanwhile, the unemployment rate dropped to 4.1%, down from 4.2%, defying expectations of it remaining steady at 4.2% and avoiding the risk of an increase to 4.3%. Wage growth registered at 0.3% month-over-month, with the annual rate easing to 3.9% from 4%. The data supports the likelihood that the Federal Reserve will maintain interest rates unchanged later this month. With two more payroll reports due before the crucial March FOMC meeting and annual benchmark revisions expected next month—likely to result in notable downward adjustments—the recent data trend reinforces market expectations of an extended pause by the Fed. This sentiment could strengthen further if core inflation next week again posts a 0.3% month-on-month increase for the fifth consecutive month. However, we reiterate a 4% target for the Fed Fund Rate in 2025, but it will be lengthened to 4Q2025.

Dollar strength may continue to strengthen past 110.00 and reach 112.00 going forward, after reaching our major target at 108.00. We also reiterate our view that there may be a reversal at 112.00 after Trump take office one to two weeks in. Which resembles the sell-off in early 2016.

Bank of Japan is now at a cross road despite rises in wage growth and inflationary pressure

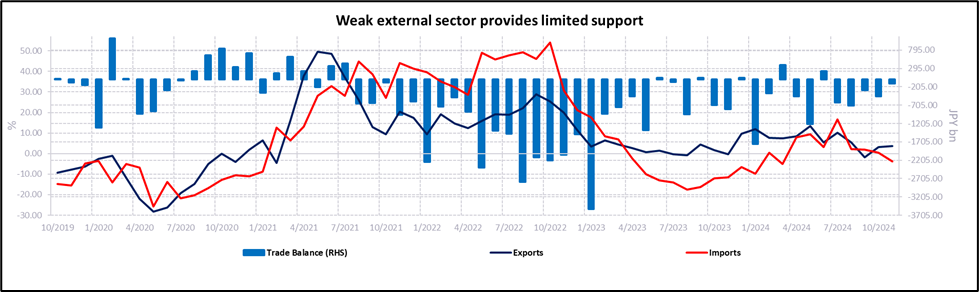

The Japanese enjoyed a raise in wage growth but 2% inflation rate has net the wage growth effect in terms of purchasing power as Tokyo’s core inflation rose 2.4%YoY. Softer export also take a toll on the export oriented economy. While BOJ’s rate hike may seems to be an unknown due to the Federal reserve’s no rate hike in January and a Trump’s presidency on trade tariffs may spurs Ueda’s consideration of a no hike in January. If that’s the scenario, the rate hike by the BOJ may be delayed till March 2025.

The near-term target of USDJPY at 157.00 has been achieved. With the uncertainty on the BOJ, we believe near-term correction is likely to be mild and will be supported at 154.62.

Uncertainty clouding the Bank of England, rate cut is out for now.

The Bank of England is battling one of the toughest time now. Sticky inflation, hindered spending by the government and the elevated US dollar rate has caused the pressure on the pound. Which we believe is one of the crucial factor which the Bank of England has turned dovish.

To add fuel to the fire, Gilt yields have surged significantly in recent months, with the 30-year yield reaching 5.3%, its highest level since 1998. The 10-year yield has also risen sharply, though at 4.7%, it remains within the range seen in the early 2000s. Factors driving this upward movement include Labour’s spending plans, persistent inflation, higher US rates, and supply pressures. While we anticipate gilt yields to decline later in the year, these contributing factors are likely to persist, delaying a reversal.

As such, we remain bearish on GBPUSD with a near-term target of 1.2000.

Summary

The dollar strength is likely to sustain in the near-term and with the interest rate of the dollar remaining relatively strong, the rest of the G5 currencies are likely to continue to weakened. As such, we remain short on AUDUSD, EURUSD, GBPUSD. Remain buy on USDJPY, USDCAD. Cross pair strategies include short on GBPJPY and GBPAUD, on the account of weaker Cable ahead.

Figure 1- Weak export by the Japanese

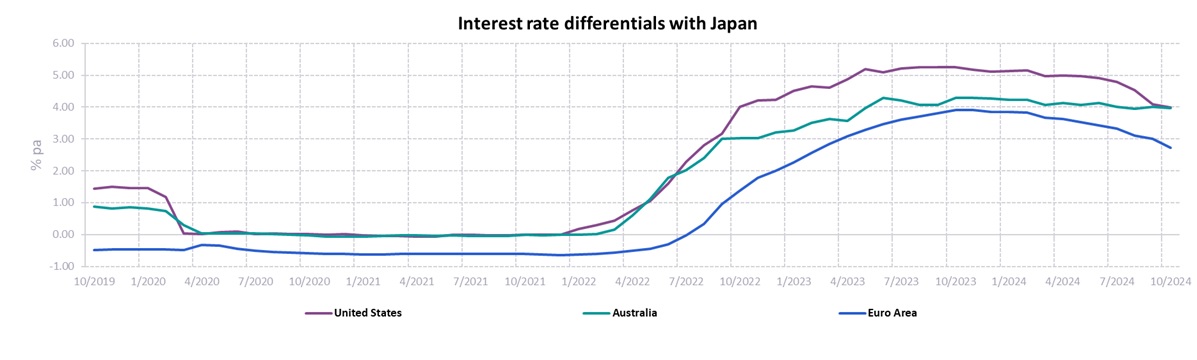

Figure 2 – Interest rate difference with major economies (Australia, Eurozone and United States)

Figure 3 – US unemployment rate normalised

Please refer to the disclaimer here.