- The US dollar maintained its strength as expected from our last report dated 16 Sep 24 as dollar remained well supported above the 100.00 psychological level

- The dollar strength can be attributed to the risky situation in the Middle East and stronger Non-farm payroll numbers.

- Strong jobs data may signal a lower rate cut at 25 bps and Fed may tread the monetary policy into the neutral zone.

Strong job growth is looking at a possible lower rate cut at 25 bps, or no cuts at all

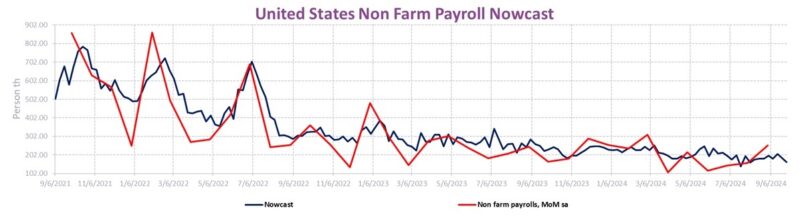

Job growth in the US has exceeded all expectations, as the September jobs report reveals a particularly strong performance. US non-farm payrolls surged by 254,000, well above the 150,000 consensus. Furthermore, the previous two months saw upward revisions totaling 72,000 (with forecasts ranging from 70,000 to 220,000). The unemployment rate declined from 4.2% to 4.1%, an outcome only one out of 71 analysts anticipated. Additionally, wages rose by 0.4% month-over-month, while August’s wage growth was revised up by 0.1 percentage point to 0.5%. Despite these strong figures which could suggest an increasing rates for the Fed, we still favor a rate cut by Powell in the upcoming FOMC in November 24.

NFP data has been inconsistent, suspect a greater revision on the next set of data

Despite data inconsistencies, we do not anticipate the Fed cutting rates by more than 25 basis points in November. The issue is that this jobs report conflicts with other key data sources. Indicators such as ISM and JOLTS number don’t tally up. Additionally, the sharp drop in the quits rate usually signals a slowdown in wage growth, not surging growth. Surveys also indicate that households perceive the labor market to be weakening, leading to skepticism about this report. Regardless, the Fed is unlikely to cut rates by 50 basis points in November. Our expectation remains a 25bps cut. Inflation data will be the next major macro data to determine the next course of rate policy.

Yen Carry trade may not be over, don’t be too happy over the weakening in Yen recently

Tourist heading to Japan for the Autumn holiday soon may see slight grin in the face after the Yen weakened slightly to 148.00 range last week. However, we believe that the Yen may continue to see further weakness and is likely to see strong rejection at 150.00. Reason being that the massive amount of the yen carry trade is relatively unknown and there is a possibility that only a fraction of it is realized. Furthermore, the Bank of Japan did not make any major changes by hiking their rates as we believe that they are wary and watching the Fed’s next step. Hence, we believe that Yen’s weakening is only temporary.

Figure 1: Non-Farm payroll has proven to be very erratic

Technical outlook on Dollar index –Corrective rebound has come to past and may break 103.00 in near term

The dollar index rebounded as expected based on our last report dated 16 Sep 24 We maintained a in view that the Dollar may see higher target towards 103.00 as strong bullish momentum has seen a strong break above the key resistance above 102.32 and the constant strong support at 100.00 gave the bulls confidence on the dollar index. Should 103.00 breaks, the next target we will be seeing will be 105.10.

.

Technical outlook on USDJPY – Upside rebound for the dollar against the Yen

The USDJPY rebounded at 140.oo psychological support and a brief upside may continues towards 150.35 in the near-term.

Below are the key pointers:

- Ichimoku saw two out of three bullish crossover and recent leading Span A is sloping up.

- Mid-term Stochastic oscillator saw an oversold crossover.

- Directional movement Index has performed a crossover near the 25-level, with the DM+ showing signs of rally. Furthermore, the ADX is sloping down, highlighting the weakening of bearish trend.

- Bullish break out of the falling wedge signal a possible bullish continuation.

Please refer to the disclaimer here.