-

The US dollar dip after Jerome Powell’s acknowledgement of a significant drop in inflation, bringing it closer to the Federal Reserve’s 2% target. Labor market weakness and concerns about employment have grown, which indicates that the economy may have been cooled and not performing as it is. He emphasized that future rate cuts will depend on data, the economic outlook, and the balance of risks. Following his comments, market participants fully priced in a rate cut for September.

-

The basis of whether is a 25bps or 50bps cut will be depending on how the unemployment rate is, should it crosses above 4.4%, the likelihood of a increased rate cut to 50bps will be higher. However, we are align with the consensus of a 25bps cut.

-

The AUD/USD pair continue to be the winner as weaker dollar and the increase in hawkishness by the Reserve Bank of Australia.

-

GBPUSD, EURUSD, USDCAD and USDJPY continues to outperform against the dollar.

Strong signal sent by Powell during Jackson hole, 25bps is set, 50bps is 50-50

Chair Powell made a strong statements in his Jackson Hole speech, highlighting that while inflation is improving and the focus has shifted more towards employment, he emphasized that “the time has come for policy to adjust” and “the direction of travel is clear.” This follows the July FOMC meeting minutes, which indicated that most members believed it would likely be appropriate to ease policy if the data continued as expected.

There was no specific discussion about whether a 25bp or 50bp rate cut would occur at the September FOMC meeting. Instead, Powell emphasized that the timing and pace of rate cuts would depend on incoming data (Especially the unemployment rate), the evolving outlook, and the balance of risks. However, he did suggest that there could be significant rate cuts if conditions warrant it, stating that the current policy rate provides ample room to respond to risks, including potential further weakening in the labor market.

Currently, the market has priced in around 25bps of cuts for the September 18 FOMC meeting, 100bps by the end of the year, and an additional 125bps next year, which seems reasonable given the situation. Before the September decision, key data releases include the core PCE deflator on August 30 and the jobs report on September 6, which is critical. Powell noted that the Fed does not seek or welcome further cooling in labor market conditions.

If the payrolls report shows a sub-100k increase and the unemployment rate rises to 4.4% or 4.5%, a 50bp cut seems more likely. If payrolls are around 150k and the unemployment rate remains at 4.3% or dips to 4.2%, a 25bp cut is expected. The core CPI on September 11 is also important, with a 0.2% MoM or lower print anticipated, possibly even 0.1% if July’s primary rent increase reverses.

Reserve Bank of Australia remains firmly hawkish, rate cut is being pushed back

The Reserve Bank of Australia (RBA) is likely to keep interest rates at their current 12-year high for an “extended period” to ensure inflation returns to its target range next year, signaling that any policy easing is still distant. According to the minutes from the RBA’s recent two-day meeting on August 20, the board considered further tightening but ultimately decided that maintaining the key rate at 4.35% was the stronger option. Members of the August 5-6 meeting noted that keeping the cash rate steady for longer than market expectations might be sufficient to bring inflation back to target within a reasonable timeframe. Despite the risk of mixed economic data, the RBA remain firmed on it interest rate policy and with a possible stronger Chinese stimulus in the economy after the Fed cuts in September, the Aussie will be the strong beneficiary over the longer-term period, which may see the Aussie reaching beyond 0.7100 against the dollar

Federal Reserve – Bank of England policy divergence signal stronger sterling

Bank of England’s Governor Andrew Bailey maintained its cool after inflation ticks up to 2.2% in July after a 25bps cut in August. Despite the unknown, Andrew Bailey has commended the significant progress made in curbing inflation in the U.K. However, he will also warn that the current monetary policy may need to stay restrictive for a longer period than previously anticipated due to ongoing challenges in the labor market. Bailey will note that the risks of persistent inflation have decreased compared to a year ago. He will express confidence in a scenario where inflation gradually subsides under the current level of monetary restriction, which would allow for a natural easing over time. Despite this optimistic outlook, Bailey will also highlight the possibility of two less favorable scenarios (Inflation pressure ticking up and labour market). In these scenarios, the Bank of England might be compelled to maintain tight monetary policy for an extended period to ensure inflation is fully brought under control.

The ECB minutes leave the possibility of a September rate cut open without making any firm commitment.

The ECB minutes reveal a more cautious stance on the growth and inflation outlook. Members acknowledged a deteriorating short-term growth outlook and expressed concern about the labor market’s resilience, which could either indicate a potential soft landing or raise doubts about the sustainability of what is seen as one of the euro area’s most inclusive and dynamic labor markets. The persistence of inflation, particularly in the services sector, remains central to the ECB’s concerns. The minutes emphasized that while progress has been made, achieving a sustainable reduction in inflation to the 2% target remains uncertain, especially given the challenges in the final stages of disinflation. There were also some reservations about the optimistic projections of slowing wage growth. Although surveys suggest a downward trend in wage growth for 2025 and 2026, the data has yet to reflect this decline, which remains historically high.

Looking ahead to the September meeting, the minutes suggest an open-minded approach, emphasizing that while data dependence is crucial, it shouldn’t lead to an overemphasis on individual data points. Overall, the minutes indicate that the ECB is more inclined towards further rate cuts and is more decisive than it was during the June meeting. The confidence that Lagarde gave is positive for the Euro against the dollar going forward.

Bank of Canada – Surprised retail sales and possible uptick in oil prices may boost demand for the loonie.

Canada saw a stronger-than-expected increase in core Retail Sales in June, but headline Retail Sales contracted as anticipated, which has kept the Canadian Dollar in good books. Economic data releases for Canada are sparse next week, with the main focus being on Friday’s update for the country’s Q2 Gross Domestic Product (GDP), which may sees continue strength going forward. Crude oil prices rebounded from the low of 71.00 and given the escalation in the middle East, oil prices may continue to rise in the mid to long-term, which could be another catalyst of stronger Loonie.

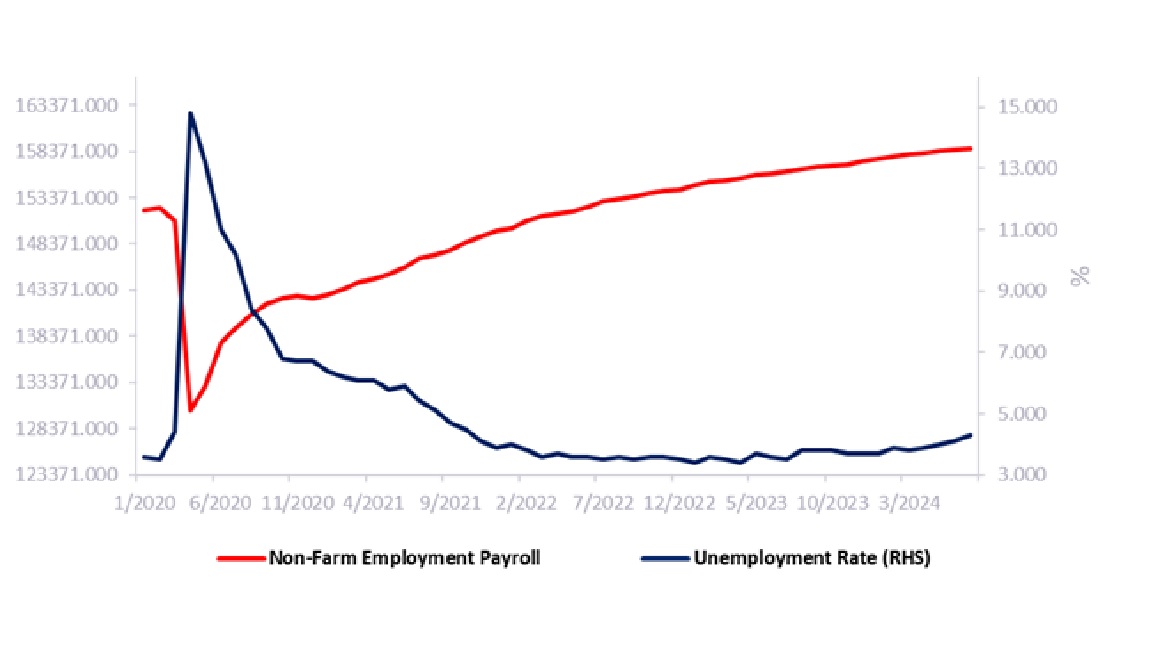

Figure 1: Unemployment rate

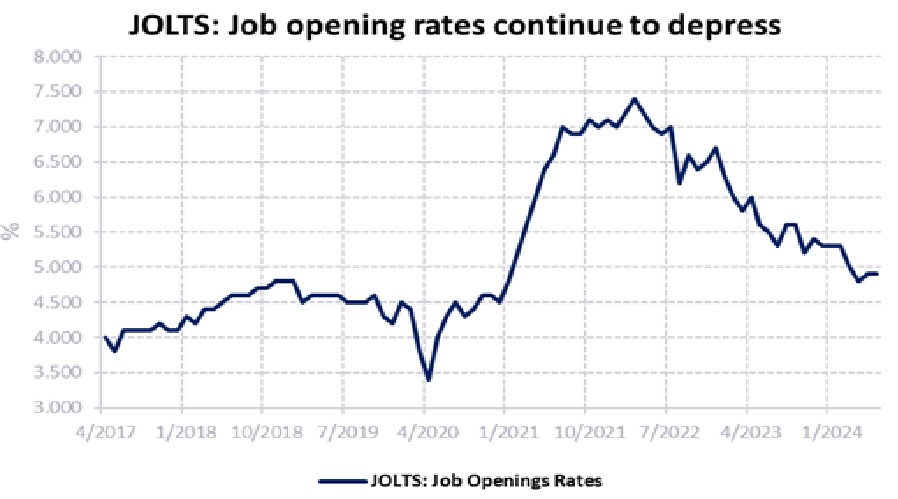

Figure 2: Job opening number continue to declined

Technical outlook on Dollar index – Strong bearish pressure

The dollar index has turned bearish and a sharp drop last Friday has signaled a possible exhaustion. Though a rebound is likely this week, it remain to be weak and may not even passed beyond 102.32 resistance. Support is at 98.45-99.56.

Technical outlook on AUDUSD – Upside momentum is strong

The Aussie dollar reached beyond our short-term target at 0.6670 and this action has conclude a possible strong break above 0.6800 resistance. Below are the key pointers highlighting the prospect of another upside:

- Ichimoku is back into the positive trend reading after prices trends above all its’ indicator.

- Long-term MACD is neutral for now but is tilting towards the bullish sentiment.

- The stochastic oscillator has confirmed the upside reversal as mentioned during our report two weeks ago.

Continue to hold on to buy for AUDUSD and watch for a rebound at 0.6600 region should a correction happens. Long-term target price is at 0.7100.

Technical outlook on GBP/USD – Attractive to buy on correction

The GBP/USD has reached our long-term target price at 1.3200 earlier than expected based on our previous outlook dated 5 Aug 24, after a sharp rebound above 1.2681 as expected. Strong momentum remains. Below are the key pointers to note:

- Ichimoku has confirmed the three bullish golden cross and GBPUSD is likely to strengthen further to the upside

- Long-term MACD is showing a clear bearish signal over the longer-term period as histogram is negative.

- Both DM+ and ADX are showing strong signs of bullish strength.

Remain buy on GBPUSD and watch for support at 1.3198 for rebound if there’s any correction. Long-term upside target is at 1.3541.

Technical outlook on EUR/USD – Strong break above 1.110

The EUR/USD has reached beyond our short-term target price at 1.0900 earlier than expected based on our previous outlook dated 5 Aug 24, after a sharp rebound above 1.0800 support where a correction was short-lived. Strong momentum remains. Below are the key pointers to note:

- Ichimoku has confirmed the three bullish golden cross and EURUSD is likely to strengthen further to the upside

- Long-term MACD is showing a clear bearish signal over the longer-term period as histogram is negative.

- Both DM+ and ADX are showing strong signs of bullish strength.

Remain buy on EURUSD and watch for support at 1.0986 for rebound if there’s any correction. Long-term upside target is at 1.1400.

Please refer to the disclaimer here.