-

The incumbent Japanese Prime Minister managed to secure his seat despite the Liberal Democratic Party (LDP) fails to secure a majority in the Diet. However, the yen retreated into weakness after Shigeru hold on to his previous stance on increasing rates on the Yen.

-

The likelihood of his reversal of stance is due to the possible uncertainty in the Trump administration next year and his election setback, which may fails to garner a strong support on BOJ hawkish stance.

-

Furthermore, the Federal Reserve will continue to go on to the path of rate cut. All eyes will be on US CPI data tomorrow.

Bank of Japan will likely maintain its target rate at 0.25%

In the final week of October 2024, the Bank of Japan maintained its policy interest rate at 0.25% and is expected to hold this rate steady at its December meeting. Despite significant growth in wages and inflationary pressures, the BOJ is unlikely to raise rates by the end of 2024. This reluctance stems in part from public dissatisfaction with rising living costs, a factor contributing to the ruling Liberal Democratic Party’s recent loss of majority in the Diet. This political shift may prompt the BOJ to adopt a cautious “wait-and-see” approach before committing to a rate increase. Additionally, Shigeru Ishiba’s recent moderation from strong yen hawkishness underscores the low likelihood of an imminent rate hike. With the LDP’s reduced majority, Ishiba may face heightened political constraints, further tempering policy adjustments.

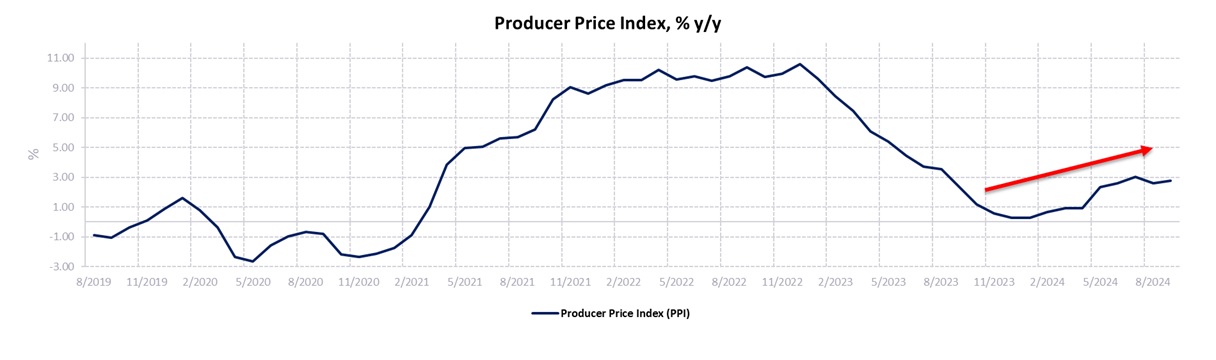

Political uncertainties, such as the potential implications of a Trump presidency in the U.S. next year and Fed Chair Jerome Powell’s guidance on dollar interest rates, add to the challenges facing the BOJ in formulating clear near-term policy. Meanwhile, rising pressures on Japan’s Producer Price Index (PPI) may influence future Consumer Price Index (CPI) figures, while deflationary trends in other major economies could afford Japan some leeway in managing inflationary concerns.

Hence, we reiterate our view that Yen is likely to weakened against the Dollar towards 157.00.

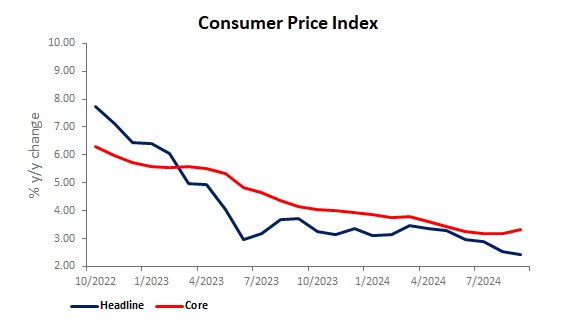

US CPI likely to see marginal increase, consensus rule it at 0.2-0.3% MoM.

The U.S. Consumer Price Index (CPI) data for October 2024 is scheduled for release on November 13, 2024, at 8:30 a.m. Eastern Time.

Current forecasts anticipate a modest month-over-month increase of approximately 0.2% to 0.3%. This projection reflects the influence of declining oil and energy prices, which are expected to offset rising costs in food and services sectors.

Should the CPI data align with these expectations, it may reinforce the Federal Reserve’s inclination toward a rate cut in December. Consequently, we anticipate a stronger U.S. dollar in the near to mid-term, with a target level of 108.00 against major currencies.

Figure 1 – US CPI to continue on its disinflationary path over the longer-term period

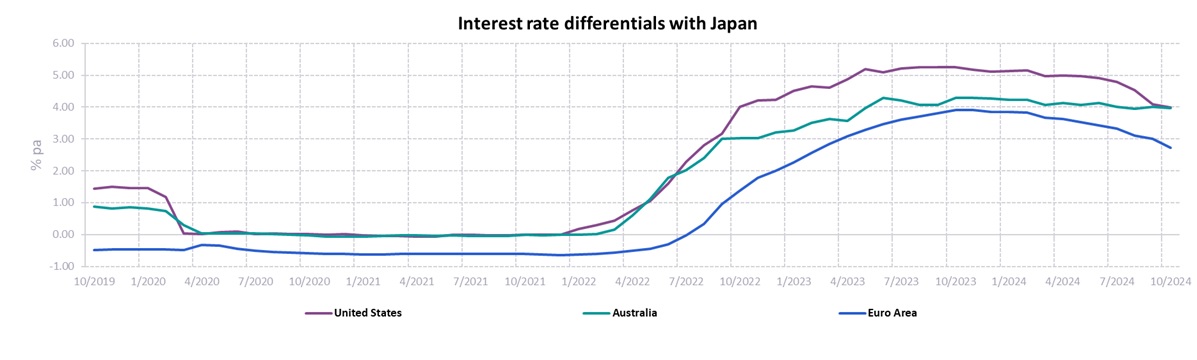

Figure 2 – Interest rate difference with major economies (Australia, Eurozone and United States)

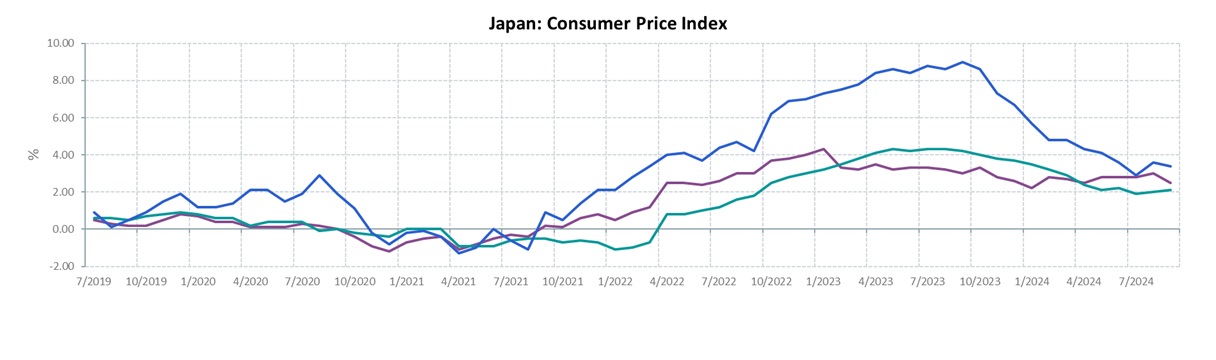

Figure 3 – Japan’s CPI may take a breather

Figure 4 – Japan’s PPI rose due to higher import cost

Please refer to the disclaimer here.