The rise of geopolitical tensions has benefitted the defense contractors. Last month, I wrote about 2 defense stocks to buy as geopolitical tensions simmer.

The article featured Lockheed Martin Corp (NYSE: LMT) and Northrop Grumman Corporation (NYSE: NOC), which have both seen their share prices soar.

It is not a surprise that investors turn towards defense stocks to avoid the volatility in the market. The prolonged conflict between Russia and Ukraine will also benefit the defense companies as countries ramp up their defense spending.

Outside of the US, BAE Systems PLC (LSE: BA) is the largest European defense contractor and I think it is a European defense stock to own for investors.

Here are 5 reasons why investors should buy BAE Systems.

1) Strong and Sustainable Dividend

Despite an increase of 49.6% in its share price over the last one year, BAE Systems’ dividend yield stood at 3.6%, which is fairly attractive.

On top of that, this is based on a cash dividend payout ratio of 37.3%. This offers a dividend safety to the company as a large portion of its cash and earnings are being retained to grow its business.

Its dividend track record is also impressive as its 5-years dividend compound annual growth rate (CAGR) stood at 3.3%.

While its dividend growth is not that impressive, its consistent dividend policy will generate investor confidence as compared to those erratic ones.

2) AUKUS Security Pact

The AUKUS Security Pact, which includes the partner nations of Australia, UK and US, working together on a defense pact involving nuclear submarines and other military capabilities, will benefit BAE Systems.

The company has a long track record in this part of the maritime market and has great relations with Australia, who are on the frontier with China.

This will allow BAE Systems to gain access to the pact’s shared technology.

3) Next-Gen Fighter Progress Smoothly Despite Brexit

BAE Systems has signed agreements for its next generation fighter, the Tempest, with partners and progress has gone smoothly without much conflict.

This is becausethe Tempest is not taking a workshare approach to the running of its programme and the roles are clearly defined.

The progress is encouraging as there were initial concerns over how Brexit might affect its next-generation fighter jet.

With few fundamental disagreements, I believe the next-generation fighter jet under BAE Systems will gain better traction as compared to its competitor in France.

4) Beneficiaries of Rising Geopolitical Tension

The Russia-Ukraine conflict has benefitted BAE Systems as seen by its share price performance.

While the current war alone do not justify buying into companies for the long-term, I believe that governments around the world will relook at their defense budget.

For example, Germany has recently unveiled a ‘new era’ in defense policy with big increase in military spending.

Aside from that, there is also the geopolitical tension between US and its allies against China. In general, the UK defenses are beneficiaries of a concerted effort to renew military alliances in direct opposition to China.

5) Attractive Valuation

BAE Systems is trading at a very attractive valuation at around 7 to 8 times on its earnings before interest, tax, depreciation and amortisation (EBITDA). This is a significant discount to its peers that are trading at a double-digit level.

Part of the reason for the lower valuation was due to the execution risks for BAE Systems. This is as the company transitions from its old Typhoon platform to the next-fighter jet for the coming decade.

Defensive Stock for Long-term Play

Overall, BAE Systems is an excellent company. It is buying back 500 million GBP of shares over the next 12 months, about 2.5% of their market cap, in addition to a growing dividend yield of 3.6%.

On top of that, the company’s prospect is promising with the rollout of its next-fighter jet, backed by tailwinds of greater UK defense cooperation and diplomatic deterioration with China.

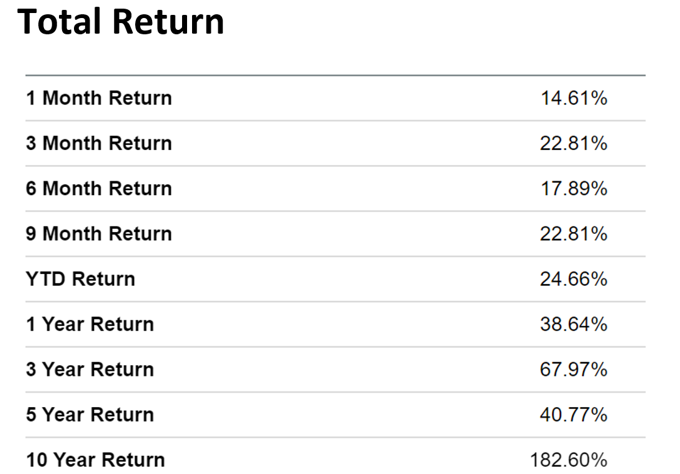

For long-term investors, BAE Systems’ total return track record will sit well with their risk appetite. Over the last 10-years, the company has generated a total return of 182.6% or a 10-year CAGR of 23.1%. While the return over the last five years have shrunk, it is still impressive at a CAGR of 7.1%.

Given the potential from an increase in military spending over the next few years, I believe BAE Systems will be a great European defense stock to buy for the long-term.

Source: SeekingAlpha, ProsperUs

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.