Travel is back in a big way, particularly for businesses in Singapore.

One of those that is always tipped to benefit is CapitaLand Ascott Trust (SGX: HMN), or CLAS for short.

The REIT reported a strong financial performance during the first half of 2023 (H1 FY2023).

While many S-REITs saw a decline in their distribution per unit (DPU), it is worth noting that CLAS demonstrated impressive growth.

It managed to post a substantial 19% year-on-year increase in its distribution per stapled security to 2.78 Singapore cents for H1 20230.

With so many uncertainties on the horizon for the global economy, here are some of the key highlights from CLAS’s latest earnings report.

Rejuvenated global travel demand drives earnings

In H1 FY2023, CLAS dazzled with a whopping 31% increase in gross profits, touching an impressive S$154.4 million.

This was in line with the sharp increase in its revenue, which witnessed a 30% year-on-year (yoy) spike to S$346.9 million.

This impressive financial gain was attributed to rejuvenated global travel demand and contributions from freshly-acquired properties.

With an extensive international portfolio that covers 107 properties across 47 cities in 15 countries – housing over 19,000 units – CLAS’s diversified reach plays a pivotal role in its financial strength.

“Twin pillars” strategy pays off

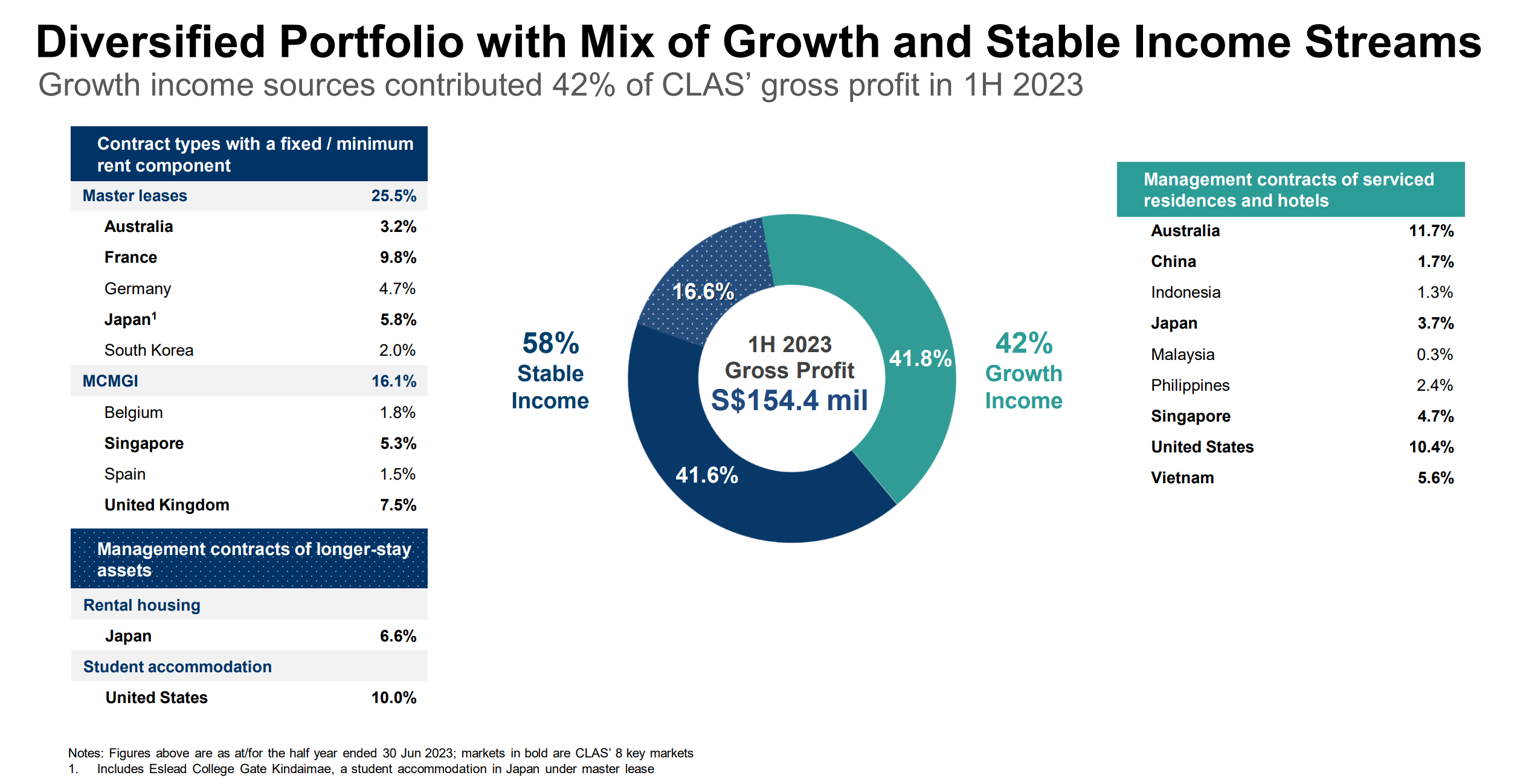

CLAS’s reliance on the “twin pillars” – growth and stable income – has helped with the earnings recovery.

The REIT’s growth income contribution in H1 FY2023 shot up to 42% from 32% in H1 FY2022, aligning with the upsurge in travel more broadly.

The trust’s portfolio includes rental housing, student accommodation, management contracts of longer-stay assets, and management contracts of serviced residences and hotels.

Source: CLAS’ H1 FY2023 Financial Results

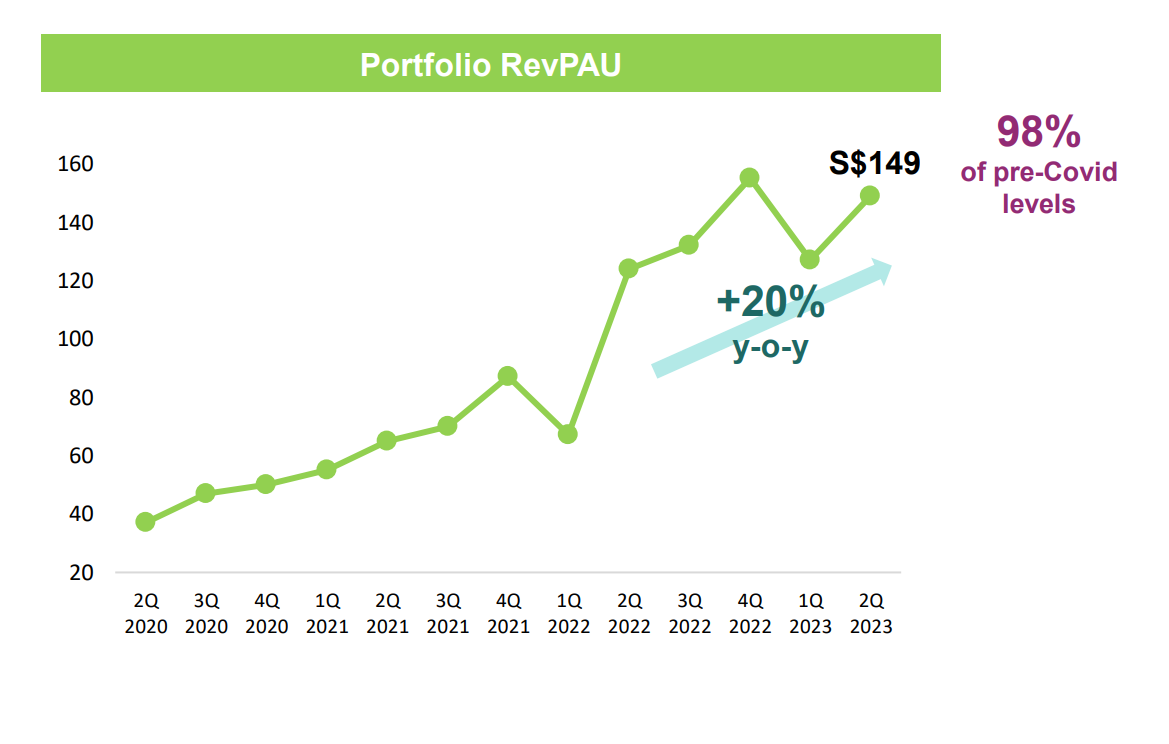

H1 FY2023’s Portfolio RevPAU surged 44%

In Q2 FY2023, CLAS’s revenue per available unit (RevPAU) for its portfolio jumped by 20% yoy.

This has helped the RevPAU to return to 98% of pre-COVID levels.

Source: CLAS’ H1 FY2023 Financial Results

Strong operating performance was primarily due to average daily rates (ADR), which surpassed pre-Covid levels.

Most of the key markets, including Australia, Japan, Singapore, the UK, and the US, have recovered to pre-COVID levels.

The strong performance was mainly led by improving flight frequencies and travel numbers globally.

Overall, the H1 FY2023 RevPAU increased by an impressive 44% compared to a year ago.

Positive forward projections

With international arrivals forecasted to bounce back to between 80% and 95% of pre-pandemic figures by the end of 2025, the future looks bright for CLAS.

Forward bookings for the third quarter of 2023 reflect increased transient demand as the summer season approaches, with a pick-up in corporate demand boosted by several events and conferences in the third quarter of 2023.

International demand is also expected to improve further in the coming months as the frequency of flights to and from China progressively recovers.

A resilient investment option

A crucial factor underpinning CLAS’s robust financial health is its multi-country portfolio, chiefly centred around the Asia Pacific region.

Its presence in pivotal domestic markets and principal gateway cities positions it to harness growth potential as travel reboots and grows.

With 70-75% of its portfolio invested in serviced residences and hotels, and 25-30% in extended-stay accommodation, CLAS stands to gain immensely from the impending travel recovery.

For dividend investors seeking a blend of stability and growth, CLAS emerges as a compelling choice.

Currently, CLAS is trading at a forward dividend yield of 5.2%.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.

")