Investors should get ready for a slew of earnings numbers coming out over the next few weeks.

For Singapore investors who have REITs, or dividend stocks in their portfolio, the earnings season has already started.

In fact, my colleague Billy touched on Q3 2022 numbers for Singapore’s biggest REIT, which reported at the end of last week.

Another large REIT here, Mapletree Logistics Trust (SGX: M44U), came out with its own Q2 FY2023 earnings yesterday (25 October).

Mapletree Logistics Trust is one of the largest REITs and a component stock of the Straits Times Index (STI).

It owns over 186 logistics properties across Singapore, Japan, Hong Kong, China, South Korea, Malaysia, Vietnam, Australia, and India.

So, how did the large pan-Asia logistics REIT perform? Here are five key takeaways for Singapore and REIT investors from Mapletree Logistics Trust’s latest earnings.

1. Revenue and profit both up double digits

Mapletree Logistics Trust saw both its revenue and net profit income (NPI), for the three months ending 30 September 2022, rise by double-digit percentages on a year-on-year basis.

Gross revenue was S$183.9 million for the quarter, up 11.4% year-on-year. Meanwhile, NPI was S$160 million, up 10.8% year-on-year.

This increase was mainly attributable to higher revenue from existing properties and contributions from accretive acquisitions, such as a logistics facility in South Korea and three logistics properties in Vietnam.

2. Average rental reversion up +3.5%

Positive rental reversion is a metric all REIT investors should watch, as it measures whether a REIT is able to raise rental prices for its properties.

In this respect, Mapletree Logistics Trust did well in its latest quarter as its portfolio had a positive rental reversion of +3.5% in its Q2 FY2023. This was up marginally from the positive +3.4% in Q1 FY 2023.

Most of the uplift for the REIT came from its properties in Australia, Singapore, Vietnam, and Japan. A further 16.3% of its rental income is up for renewal in H2 FY2023 (for the six months ending 31 March 2023).

3. Dividend down sequentially but up year-on-year

One of the big reasons we invest in REITs is for the recurring income from the portfolio of properties they own.

Mapletree Logistics Trust’s distribution per unit (DPU), otherwise known as the dividend of a REIT, came in at 2.248 Singapore cents for Q2 FY2023.

While that was up 3.5% year-on-year, it was down on a quarter-on-quarter basis by 0.9%. that’s no surprise given the rising interest rate environment and, therefore, higher cost of funding.

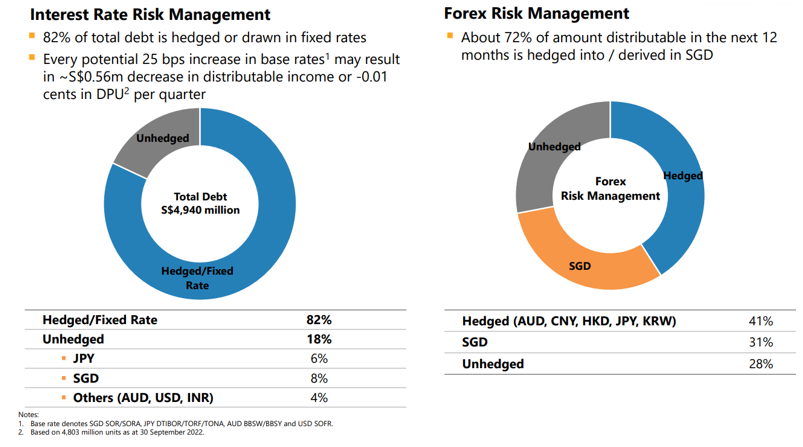

Management noted that every for every hike of 25 basis points (bps) in interest rates, the DPU would be negatively impacted by 0.01 Singapore cents.

4. Over four-fifths of debt hedged, borrowing costs up 34%

Given the way the US Federal Reserve is furiously hiking interest rates, the way REITs manage their debt load is increasingly important.

One way to do this is to hedge existing debt into fixed rates, to give the REIT visibility on debt obligations.

Mapletree Logistics Trust has done exactly this as 82% of its debt is hedged into fixed rates (see below). However, it’s also important to remember that borrowing costs also go up as interest rates rise.

Source: Mapletree Logistics Trust Q2 FY2023 earnings presentation

Source: Mapletree Logistics Trust Q2 FY2023 earnings presentation

The REIT’s borrowing costs were S$33.4 million for the quarter, up 33.7% year-on-year, driven by higher interest rates and incremental borrowings for acquisitions.

5. Overall portfolio occupancy down slightly

Portfolio occupancy for Mapletree Logistics Trust came in at 96.4% as of the end of September 2022. That was down marginally from the 96.8% occupancy rate as of the end of June 2022.

There were lower occupancies in Singapore (although this was due to several single-tenanted properties being converted to multi-tenanted ones), Japan and China.

However, this was partially offset by an improvement in occupancy rates for the REIT’s properties in Malaysia and South Korea.

Occupancy for its Vietnam, Australia, and India properties were stable quarter-on-quarter and all three had occupancy rates of 100% as of the end of September 2022.

Watch for interest rates and Asian currencies

Obviously, for all REITs, the direction and trajectory of interest rates in the US is going to be key for investor sentiment.

As for Mapletree Logistics Trust specifically, management noted that overall leasing demand in its markets remains resilient.

Higher interest rates and depreciation in regional Asian currencies (versus the Singapore dollar) were cited as key risks that could negatively affect its distributable income.

However, the fact that 72% of its distributable income over the next 12 months is hedged into Singapore dollars should offset some of these headwinds.

Management is focused on portfolio rejuvenation – via asset enhancement initiatives (AEIs) and “greening” its portfolio – along with prudent capital management.

For REIT investors, Mapletree Logistics Trust shares are currently trading at S$1.50, offering investors a 12-month forward dividend yield of 6%.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips owns shares of Mapletree Logistics Trust.