The selling pressure on Singapore real estate investment trusts (REITs) has affected the likes of the biggest and best-run REITs.

That has included CapitaLand Integrated Commercial Trust (SGX: C38U), also known as “CICT”, which is the largest listed REIT here in Singapore.

This poor performance has mainly been due to the rising interest rate environment, which makes the distribution yield of REITs less attractive given the narrowing yield spread.

However, despite losing 14.7% of its value so far this year, CICT’s earnings continue to impress as its latest Q3 FY2022 results actually surpassed its pre-pandemic levels.

The largest REIT player shows resilience

CICT is the largest REIT player in Singapore with a market capitalisation of S$12 billion.

It is the third-largest REIT in Asia Pacific and was formed following the merger of CapitaLand Commercial Trust (CCT) and CapitaLand Mall Trust (CMT).

It is backed by its sponsor, CapitaLand Investment Ltd (SGX: 9CI), and has Temasek Holdings as a major shareholder.

The retail and commercial REIT has 21 properties in Singapore, two in Germany and three in Australia.

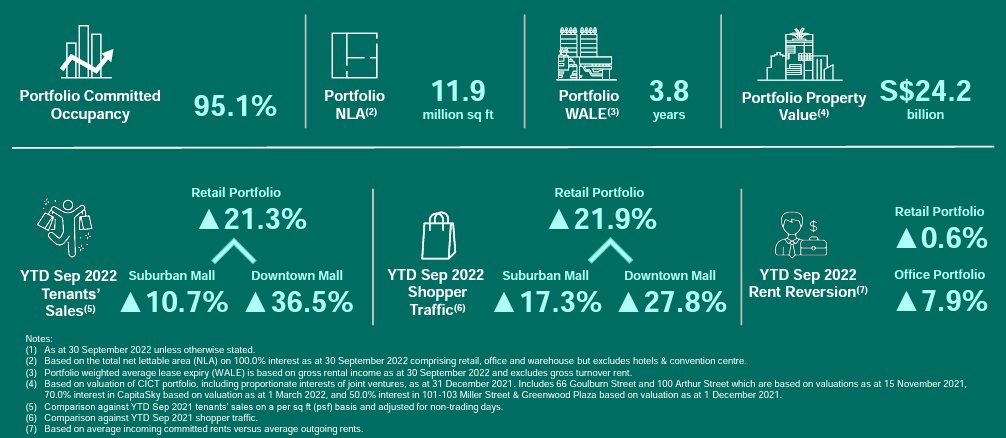

The latest results earnings reflect the resilience of CICT’s portfolio – especially in Singapore.

During the third quarter, retail rent reversions turned positive with a 1.2% gain, while its Singapore office portfolio saw a strong recovery.

Occupancies jumped over 90% and that helped increase total portfolio occupancy to 95.1%, from 93.1% in Q2 FY2022.

Profit surpassed pre-COVID levels

Net property income (NPI) increased by 12.7% year-on-year (yoy) to S$273.3 million in Q3 FY2022, supported by new acquisitions and higher revenue on gross turnover.

This was partially offset by the rise in utilities expenses.

Source: Source: CICT’s Q3 2022 Business Update

When you look at the operational metrics of CICT in Q3 FY2022, you will notice an improvement across the board with portfolio occupancy increasing to 95.1% while tenants’ sales have surpassed its 2019 levels.

This shows that most of the tenants have seen recovery to pre-COVID levels and there is also a positive trend in the signing of rents during Q3 FY2022.

Source: CICT’s 3Q 2022 Business Update

Source: CICT’s 3Q 2022 Business Update

Rising interest rates will cut DPU

CICT has locked in 80% of its borrowings on fixed rates with a low average cost of debt of 2.5%.

Its average term to maturity is at 4.1 years, allowing CICT to manage the rising interest rate environment better.

So far this year, CICT has secured S$2.7 billion of sustainability-linked, or green, bonds and loan facilities, bringing total outstanding sustainability-linked or green debt to S$3.2 billion as of 30 September 2022.

In terms of the impact of the rising interest rate environment, management has guided an additional annual interest expense of S$19.97 million – assuming an increase of 1.0% in interest rates.

Buy CICT for the steady income

It is unavoidable for unit prices to come down amid the rising interest rate environment.

The lower risk premium and valuation will naturally make REITs less attractive as compared to other yielding asset classes.

However, if you want to tap the potential growth of the commercial property sector in Singapore, CICT is a proxy that allows you to gain exposure.

With a 12-month forward distribution yield of 5.7%, this allows you to enjoy a steady recurring income over the long term.

Given the size of its asset base, the support of its sponsor and shareholder, its well-diversified funding and its resilient earnings, I believe that long-term investors will find CICT to be a good addition to their portfolio.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.