For any long-term investor interested in the world of software and the Software-as-a-Service (SaaS) business model, then they’ll know that Salesforce.com Inc (NYSE: CRM) founder Marc Benioff plays a key role in its ascendancy.

Charging a subscription fee for software delivered remotely was something that enterprise-focused, cloud-based customer management service provider Salesforce first pioneered.

And the company, which competes with the likes of Microsoft Corporation (NASDAQ: MSFT) for business, released its second-quarter fiscal year (FY) 2022 earnings on Wednesday.

Salesforce continues to show why it’s a leader in the enterprise software realm. For the three months ending 31 July, Salesforce generated revenue of US$6.34 billion – which was a 23% year-on-year increase from the year-ago period.

Generating that recurring revenue

For SaaS companies, one of their key advantages is that they are a “win-win” business for both the actual company and its clients.

While offering flexibility in pricing, on affordable monthly or annual plans, as well as the chance to test the product out on a free trial, businesses are much more inclined to spend on software when the capital outlay required isn’t a significant.

On the business side, it offers companies such as Salesforce the ability to better price its products and scale them profitably.

But perhaps the key point is that the regularity of the revenue generated means sales visibility for SaaS companies is extremely high when looking out into the future – granted that the firm is offering a “must-have” rather than “nice-to-have” software product to clients.

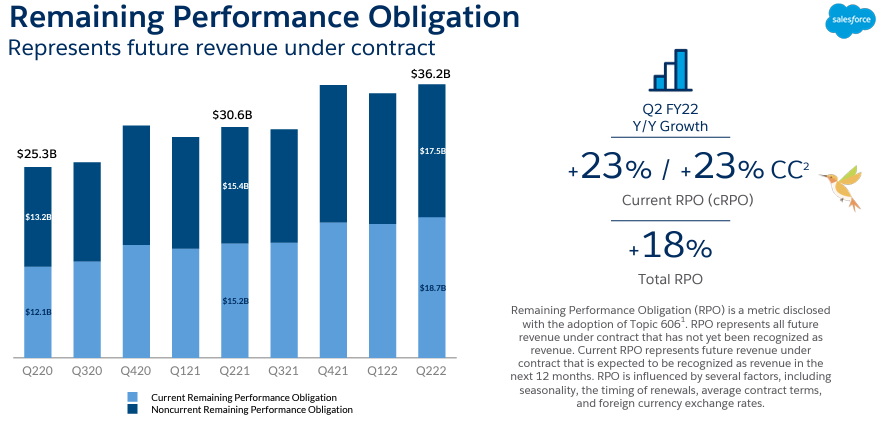

How do you tell this? Look at the remaining performance obligations (RPO), which is a key metric for understanding the backlog in revenue (from agreed contracts) that has yet to be officially recognised as revenue.

Think of it as “deferred revenue” which will feature on the company’s top line numbers some point in the future and is generally seen as a key indicator of the momentum of SaaS businesses.

On this front, Salesforce continues to “knock it out of the park” on the RPO measure (see below). Salesforce saw a robust near-20% year-on-year growth in RPO to US$36.2 billion.

With the company having just completed its US$27.7 billion deal for previously-listed workplace productivity tool Slack Technologies Inc, Salesforce is determined to keep fighting Microsoft to the enterprise software crown.

Source: Salesforce.com Q2 FY 2022 earnings presentation

Disclaimer: ProsperUs Head of Content Tim Phillips owns shares of Microsoft Corporation.