If you’re an investor and you haven’t heard of the Chinese government’s crackdown on the technology sector, then you must be living under a rock.

Well, earlier this week, WeChat and online gaming giant Tencent Holdings Ltd (SEHK: 700) reported its latest second-quarter 2021 earnings.

As usual, they didn’t fail to impress although this time the numbers were clouded by the dark silhouette of government regulation that hangs over the company.

Structural rerating?

For Tencent, total revenue in the second quarter of the year hit RMB 138.3 billion (US$21.3 billion), up 20% year-on-year, while net profit attributable to shareholders rose to RMB 34 billion – up 13% year-on-year.

Even better, the network effect of its monster WeChat app continued to dominate as users of its chat app hit 1.25 billion as of the end of the second quarter.

Yet, does all that really matter in the grand scheme of things? A lot of China market watchers have been saying that fundamentals carry less importance now when government regulation can instantly sweep away certain growth areas.

What will be more interesting, at least for long-term investors, is when this will eventually shake out and at what point confidence is restored enough to buy the tech giants once more at these depressed valuations.

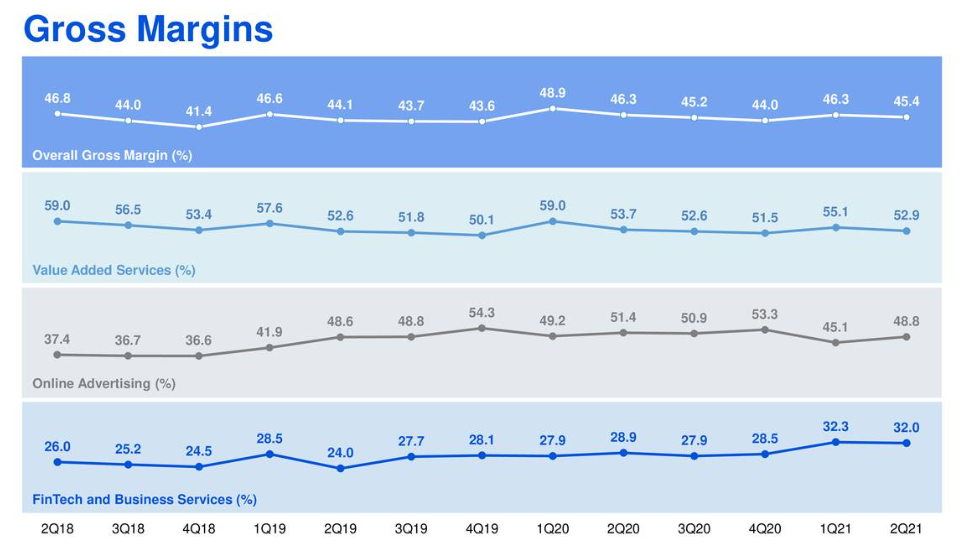

One key metric to watch will be Tencent’s gross margins (see below), where there has been extraordinary stability since 2019.

There was some margin compression during 2018 when, if investors recall, Chinese regulators clamped down on the new release of online games in China.

That saw its higher margin games business (in the Value Added Services segment) see margins get squeezed.

With new regulations coming in, and Beijing’s watchful eye ensuring competition is freed up, expect margins to potentially fall in the years to come.

Sources: Tencent Q2 2021 earnings presentation

Sources: Tencent Q2 2021 earnings presentation

Disclaimer: ProsperUs Head of Content Tim Phillips doesn’t own shares of any companies mentioned.