In the US, banks experienced a favourable tailwind from increased interest rates during the second quarter of 2023.

This boost contributed to significant upward movements in major financial indices and large banking stocks.

However, the financial horizon isn’t entirely sunny, with challenges such as decreased consumer expenditure, decelerated loan expansion, and escalating costs associated with deposit retention putting a dampener on the sector’s future prospects.

With all that in mind, here are five key takeaways from the latest earnings reported by US banks.

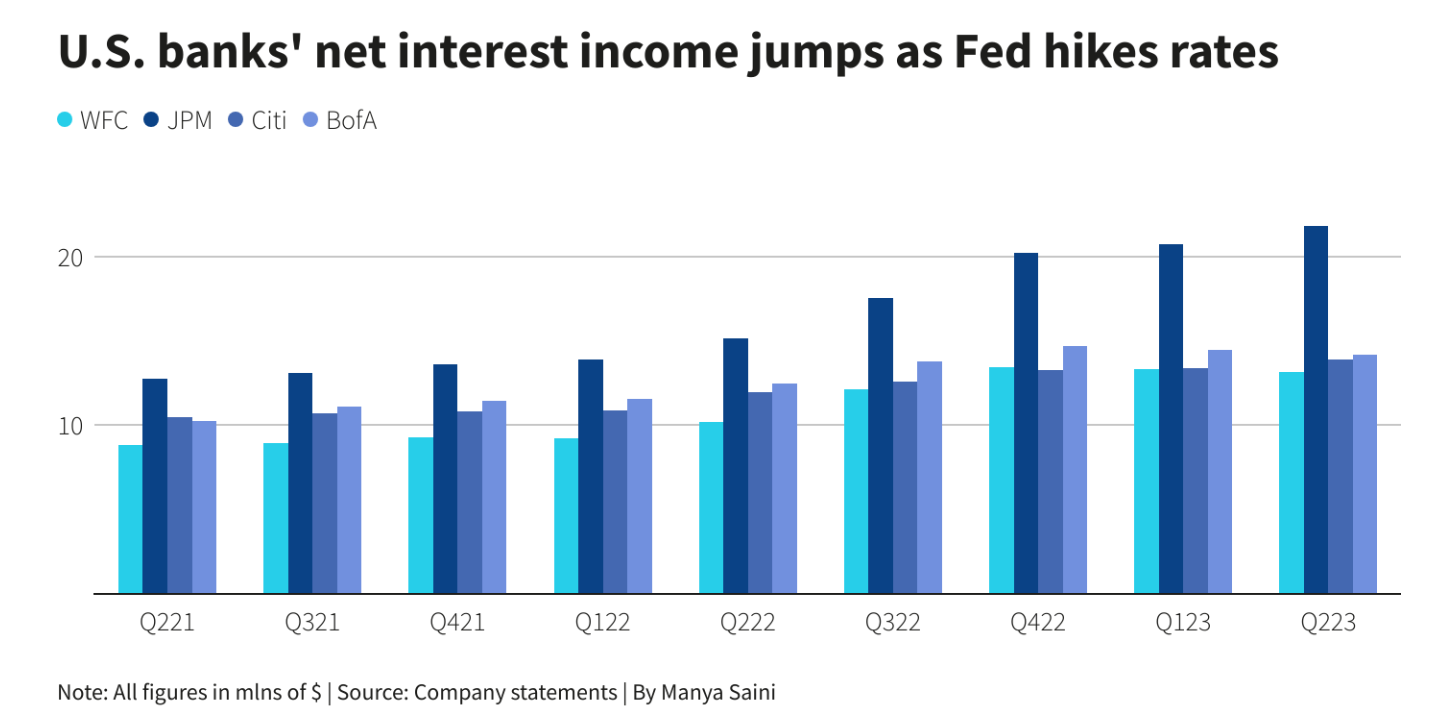

1. Rising net interest income but potential plateau

The leading US banks enjoyed an increase in net interest income (NII), which represents the gap between loan charges and deposit payouts.

This uptick was largely due to raised interest rates by the US Federal Reserve.

However, as we are near the end of the US Fed’s tightening cycle, the expansion in its net interest margin (NIM) is likely to dissipate and normalise going forward.

2. Muted loan growth but recovery in fee contributions

Meanwhile, loan growth in the US remains subdued with a linked-quarter growth of 1.6%.

The marginal increase is in line with the prevailing interest rate pressures.

As for the fee contributions, there were signs of recovery as fee contributions rebounded by 4.9% from the previous quarter, offering a silver lining and a potential recovery going forward.

3. Deposit level reported slight decline but averted crisis

The majority of prominent lenders saw a slight reduction in their deposit levels.

After the shocking collapse of three banks earlier this year, the stability and cost-efficiency of deposit retention have come under close investor scrutiny.

Recent results from regional banks have provided some assurances to investors, signalling the subsiding of the earlier crisis.

However, banks continue to face challenges as they up their deposit offerings to retain customers.

This could potentially dent their profit margins in the near term as the interest rate hike cycle is near its end.

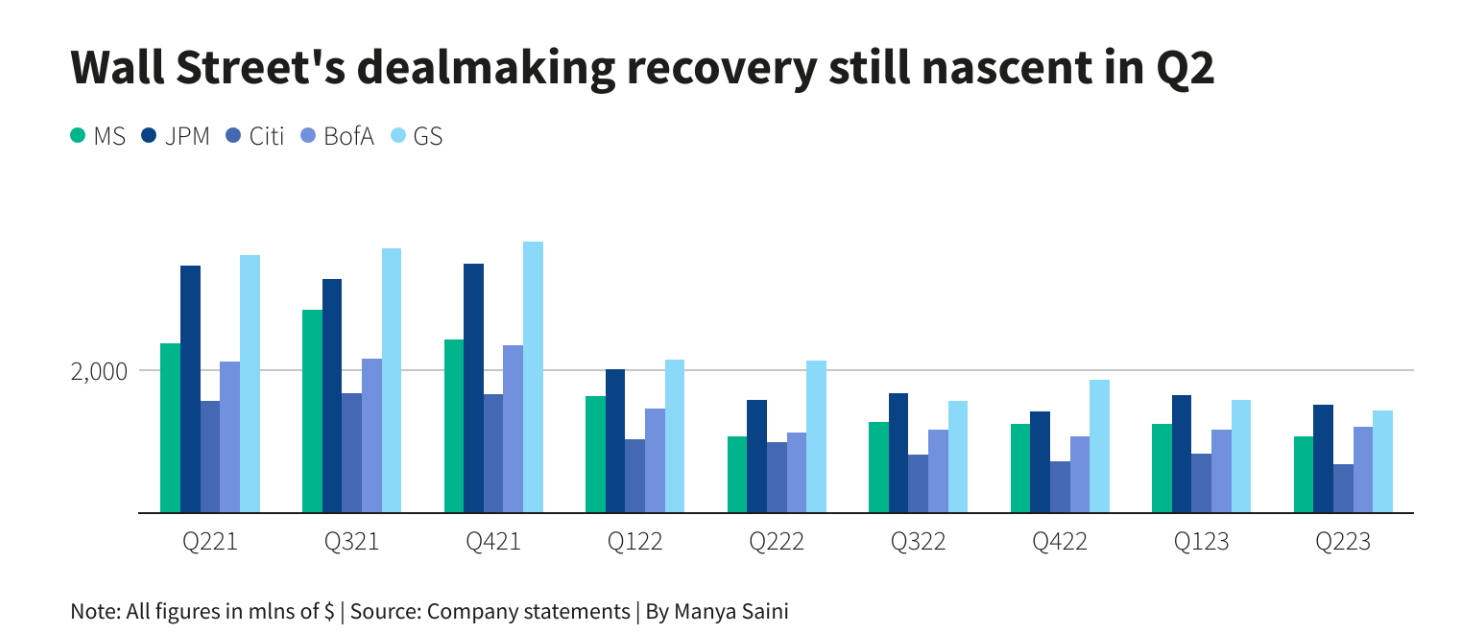

4. Investment activities remained slow

Major US banking players unveiled a wide spectrum of Q2 2023 outcomes in investment banking.

The results showed a slow recovery in investment activities but investor sentiment leans towards a positive recovery in the second half of this year.

Bank of America Corp (NYSE: BAC) emerged as a standout, surpassing its counterparts with unexpected gains in Q2 2023 investment banking fees.

5. Credit metrics remain stable but uncertainty looms large

Economic health concerns have heightened post the banking crisis earlier this year.

Commercial Real Estate (CRE) loan portfolios are under scrutiny within the banking sphere, especially those related to office spaces.

As remote working trends persist, many office structures face financial strains due to increased vacancies.

However, credit metrics seem stable, with Non-Performing Assets (NPAs) to Loans stable at 0.38%, and median Net Charge-Offs (NCOs) to Loans lingering at a low of 0.05%.

But the shadow of uncertainty looms, especially as allowance levels have increased and provision growth rose by 12.3%.

Banks beat expectations in Q2 2023

After a turbulent first quarter, marked by the failure of Silicon Valley Bank as well as two other lenders, Q2 2023 showed initial glimpses of rejuvenation in the investment banking sphere.

As the first full week of the Q2 2023 bank earnings season concludes, we saw that about 57% of the reporting banks have managed to surpass consensus expectations, a marked improvement over the 51% from the preceding quarter.

However, this is still short of the 64% beat rate achieved during the same period last year.

This resurgence, attributed to the adverse effects of heightened interest rates and looming economic uncertainty on trading and deals, has propelled bank stocks upward.

As the banking sector navigates the myriad challenges and opportunities of Q2 2023, it is clear that adaptability and resilience will be key.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.