Singapore Exchange Limited (SGX: S68) is Singapore’s only stock exchange operator, which gives them a natural monopoly.

This week, Singapore Exchange, or SGX for short, reported its H1FY2023 earnings, which saw an increase of 7% year-on-year (yoy) in its adjusted net profit to S$236.8 million.

Revenue was up by 10% to S$571.4 million during the same period.

I have shared about SGX being one of the long-term investment picks for investors back in August last year.

With the strong earnings reported despite of the challenging macroenvironment, here are three key takeaways for investors looking to invest in SGX.

1. SGX’s multi-asset platform attracts global investors amid market volatility

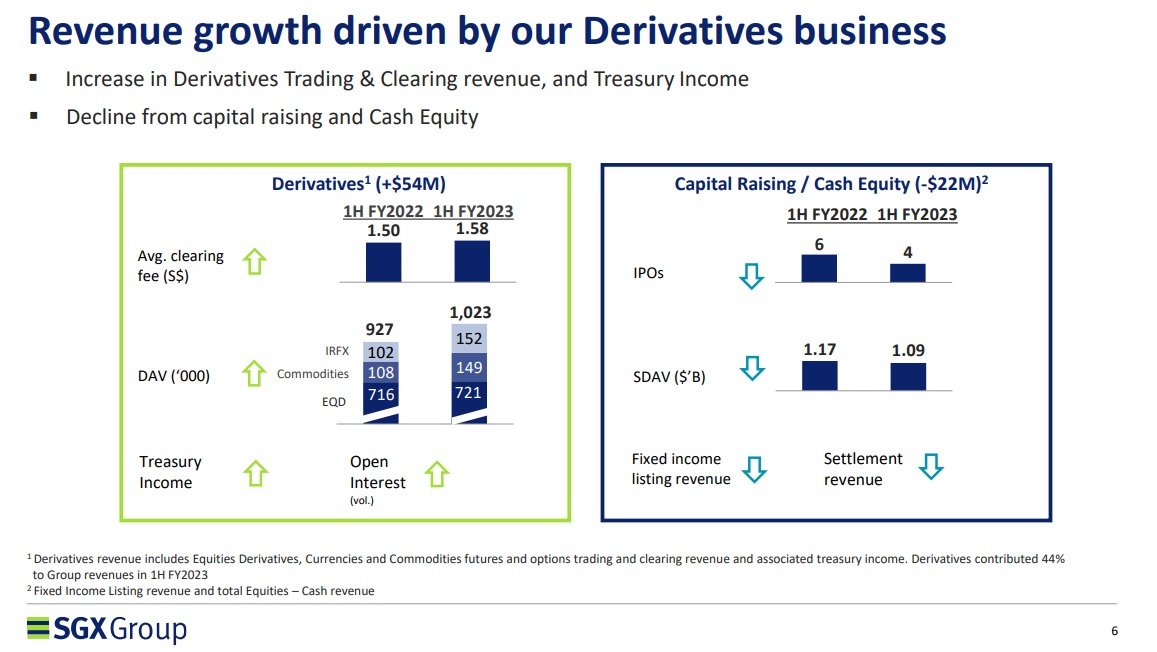

One of the key highlights from SGX’s earnings is the strong derivatives trading volume amid the heightened market volatility.

Source: SGX H1 FY2023 Financial Highlights and Performance

According to SGX’s CEO, Loh Boon Chye, the Group’s derivatives business continued to outperform with a 28% yoy increase in revenue, driven by broad-based gains across asset classes and record volumes in key contracts.

Derivatives contributed about 44% to SGX’s total revenue. The outperformance of the derivatives business reflects the value of SGX as a platform for Asian access and portfolio risk management.

SGX’s multi-asset platform continues to be a popular choice for global investors amid the market volatility. Daily average volume (DAV) rose 10% yoy to over 1 million contracts in the H1 FY2023 with growth seen across all three key areas, namely, equities, foreign exchange and commodities.

With the market remaining uncertain over the US Federal Reserve rate hikes and a potential global recession, I believe that SGX will continue to benefit from the increased activity in risk management across the region.

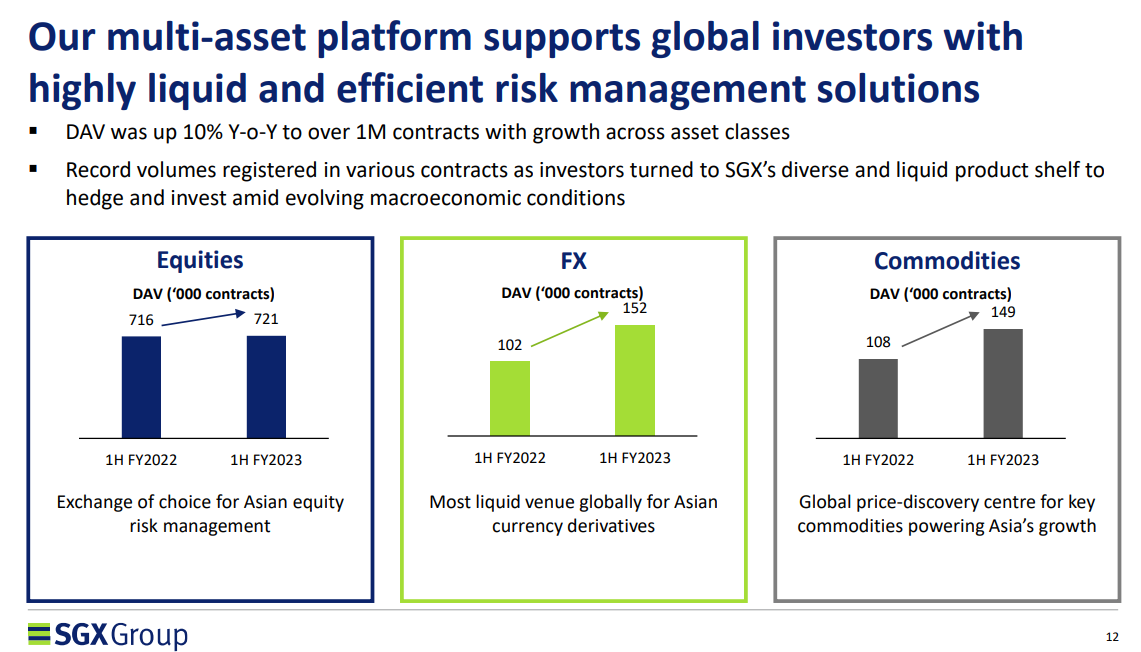

2. Beneficiary of the reopening in China

Source: SGX H1 FY2023 Financial Highlights and Performance

The outlook for SGX is also positive especially with the reopening in China, which is expected to lead to higher portfolio risk management and access activities into SGX’s derivatives platform.

Guidance for FY2023 expenses and capital expenditure remains unchanged but the stock exchange operator expects full expense growth and capital expenditure to be at the lower-end of its earlier guidance of a 7%-9% increase and S$70 million-S$75 million respectively.

Growth momentum seen in products such as steel and iron ore derivatives trading is also expected to continue going forward.

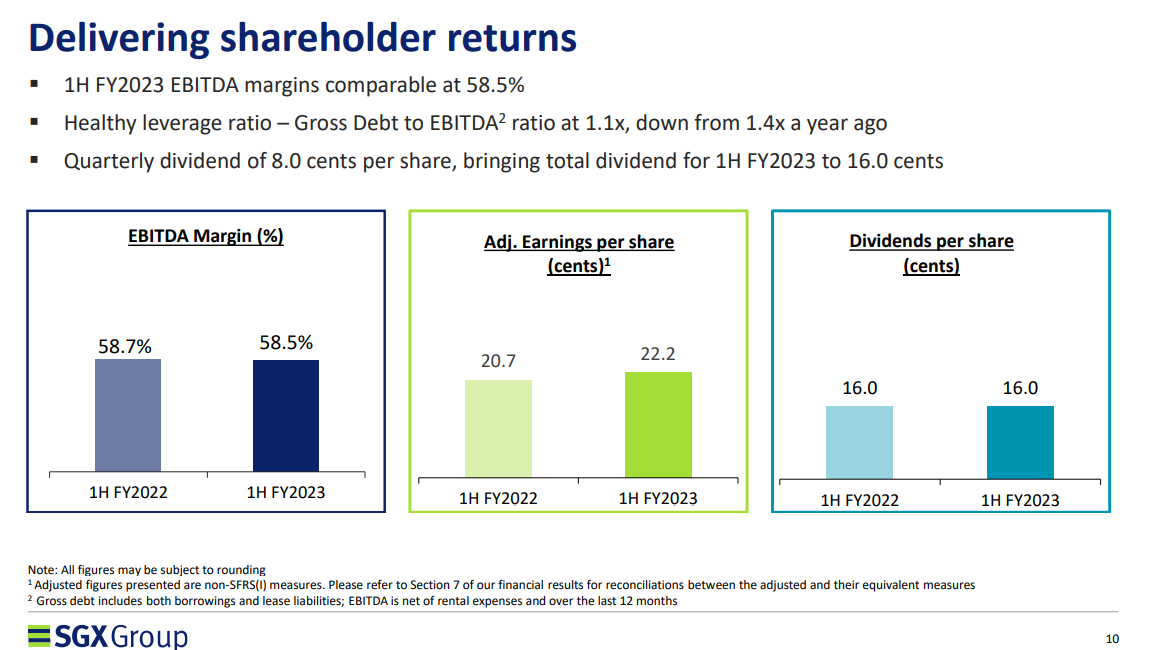

3. Consistent dividend payout with strong positive cash flow

Source: SGX H1 FY2023 Financial Highlights and Performance

SGX also rewards its shareholders with consistent dividend payout.

The bourse operator declared an interim dividend of S$0.08, bringing 1H FY2023’s dividend to S$0.16.

The latest dividend will be paid out on 24 February.

This is in line with the strong financial performance of the Group.

In the H1 FY2023, SGX’s earnings before interest, tax, depreciation and amortization (EBITDA) margin remains comparable at 58.5% as compared to 58.7% in H1 FY2022 despite of the rising cost.

It also has a healthy leverage ratio with gross debt-to-EBITDA ratio moderated to 1.1x in H1 FY2023 as compared to 1.4x in H1 FY2022.

With a healthy balance sheet and a free cash flow of S$163.1 million in the H1 FY2023, SGX is in a strong position to maintain its current dividend.

SGX continues to innovate with regional links

SGX has set itself apart in the region with its multi-asset platform that attracts global investors.

Going forward, there will be more innovation as SGX strengthens its regional links and deepens access with leading economies in the region.

Among some of those include the National Stock Exchange of India IFSC-SGX Connect.

Growth has so far exceeded expectations and with a strong dividend track record and reputation, I believe investors should consider SGX as part of their long-term portfolio.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.