In Singapore, the big banks dominate the stock market and the benchmark Straits Times Index (STI).

Many investors also buy shares of Singapore banks for their generous dividends which, in this environment of higher interest rates, they’ve been raising.

With the banks reporting their latest earnings, the country’s largest – DBS Group Holdings Ltd (SGX: D05) – unveiled its Q2 2023 and H1 2023 results on Thursday (3 August).

With a lot of investor expectation in the run-up to DBS’s results, here are some of the key highlights of the bank’s latest earnings.

DBS net profit reaches record high

For Q2 2023, DBS posted a record net profit of S$2.69 billion – up 48% year-on-year. This was 11% ahead of consensus estimates of S$2.42 billion, so in that sense it was an easy beat.

Meanwhile, its return on equity (ROE) for Q2 2023 hit 19.2% as total income crossed the S$5 billion threshold over the period.

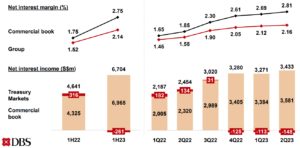

Net interest margin (NIM) for DBS actually rose by 4 basis points (bps) quarter-on-quarter in Q2 2023 to 2.16% (see below), coming in ahead of expectations as net interest income (NII) hit S$3.4 billion for the period.

Source: DBS Group’s Q2 2023 and H1 2023 CFO earnings presentation

For the whole of H1 2023, DBS saw NIM of 2.14% and NII of S$6.7 billion, both up substantially from H1 2022. Its first-half 2023 net profit of S$5.26 billion was also a record high, soaring 45% year-on-year.

Dividend hike surprise by DBS

For shareholders, there was more positive news from the earnings beat that DBS posted. And that came in the form of a higher dividend per share (DPS).

While DBS paid out a DPS of 42 Singapore cents for Q1 2023, the expectation was that the bank would keep it steady at that rate.

However, DBS raised its dividend to 48 Singapore cents, representing a 14% quarter-on-quarter increase.

DBS CEO Piyush Gupta said, in prepared remarks, that the higher dividend reflects the “stronger growth prospects for the year”.

It’s also in line with the guidance for the baseline annual increase of 24 cents per share. He also added that there was upside to this depending on business conditions and the macroeconomic outlook.

DBS also guided for the deployment to shareholders of an extra S$3 billion if it brings its CET-1 operating range down to 12.5-13.5%.

This could come in the form of a step-up in the ordinary dividend, a special dividend or share buybacks.

Citi Taiwan integration on track

DBS did also provide an update on its acquisition of Citigroup Inc’s (NYSE: C) Taiwan retail business.

Management said that it expects DBS to complete the integration of Citi’s Taiwan retail franchise – into its own operations – by the middle of this month (August 2023).

The bank also guided for an additional S$60 million in integration costs for H2 2023 but the business there should contribute around S$50 million to the bottom line for this year and around S$200-250 million in 2024.

Elsewhere, DBS’s non-performing loan ratio (NPL) remained constant at 1.1% and it had a strong CET-1 ratio of 14.1% as of the end of June 2023.

Robust quarter from DBS but watch Fed moves

It was another solid quarter from DBS, easily beating expectations, along with a nice dividend surprise for investors.

However, with the US Federal Reserve (Fed) looking like it could be finishing up with rate hikes, DBS’s NII and NIM could start to peak in the second half of 2023.

That’s offset by potential for DBS to pull other levers in its business to keep growing, such as wealth management and credit card fee income.

But investors should remember that if the Fed starts to cut interest rates in 2024 then that would reduce the potential profits of big banks like DBS.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips owns shares in DBS Group Holdings Ltd.