If you’re living in Southeast Asia, you’ve probably used one of the many mobility services that Grab Holdings Ltd (NASDAQ: GRAB) has to offer.

These can range from ride-hailing and food delivery to tailored express delivery services, many of which Singapore residents will be familiar with.

The company went public via a SPAC in December 2021 but since then its shares have tumbled over 50% from where they ended their first day.

That’s mainly been down to higher interest rates and the reset of share prices for many growthy stocks. However, Grab has also faced a challenge trying to prove to shareholders that it can scale profitably.

Grab, which is headquartered in the Lion City, reported its Q2 2023 earnings in late August. Here’s what shareholders and investors need to know.

Grab’s GMV pace picks up while revenue growth still strong

Coming into the earnings release, there were worries about the strength of the consumer in ASEAN. However, Grab managed to dispel any lingering fears by posting robust 77% year-on-year growth in revenue to US$567 million.

The mobility firm’s gross merchandise value (GMV) – which measures the total value of goods and services sold on its platforms – rose by 4% year-on-year to US$5.24 billion.

That figure was slightly ahead of the 3% GMV growth that it posted in Q1 2023.

What really helped the stock soar over 10% following the earnings announcement was the fact that Grab altered its outlook to say that its FY2023 adjusted EBITDA loss would only be US$30-40 million, down significantly from its previous forecast of US$195-235 million.

Furthermore, management predicts that it will reach adjusted EBITDA breakeven in Q3 of this year versus prior projections of Q4.

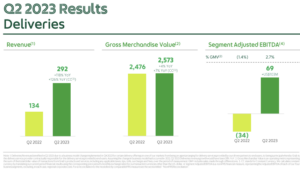

Deliveries taking centre stage for Grab

One interesting fact about Grab’s business is that its Deliveries segment is now the company’s biggest revenue generator and growth provider, too.

As readers can see below, revenue for the segment soared 118% year-on-year to US$292 million. This compared to the 29% year-on-year growth in revenue for its Mobility business, which generated US$208 million in revenue during Q2 2023.

Source: Grab Q2 2023 earnings presentation

It’s also becoming a much bigger contributor to overall profits, as it swung to a segment adjusted EBITDA profit of US$69 million in Q2 2023.

However, Grab’s Mobility division is still its most profitable given the US$163 million segment adjusted EBITDA for the division during the period.

Longer term profitability still a question for Grab

However, as is the case with most Southeast Asian tech stocks, the question of both sustainable and profitable growth is still up in the air.

One thing to note is the amount of “incentives” still on offer by Grab, both to its driver- and merchant-partners as well as consumers.

In Q2 2023 alone, “excess incentives” and “consumer incentives” came to a total of US$348 million. Consumer incentives in its Deliveries segment was a particular culprit, making up US$173 million of that number.

While the overall figure was down from the combined US$474 million for these two segments in Q2 2022, it’s still a decent amount of money that’s going towards incentives.

Overall, though, investors liked Grab’s latest earnings report and shares are now up around 11% so far in 2023.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips doesn’t own shares of any companies mentioned.