In Singapore, the earnings season for real estate investment trusts (REITs) has started in earnest. The Federal Reserve (Fed) is raising interest rates given higher inflation in the US and this has caused concern on the prospects of growth stocks.

In Singapore’s case, it has also shone a spotlight on REITs given their reliance on cheap debt to fund the growth of their portfolios.

As my colleague Billy pointed out in his article on inflation, prices in the Lion City are also rising – with the headline consumer price index (CPI) hitting a nine-year high of 4% in December.

So, with that, the upcoming earnings season is important to understand how the local REIT sector is doing. One of the first large REITs to report was healthcare-focused Parkway Life REIT (SGX: C2PU).

Here’s what dividend investors in Singapore should know about the healthcare REIT’s latest fourth-quarter and full-year 2021 earnings.

Rising DPU

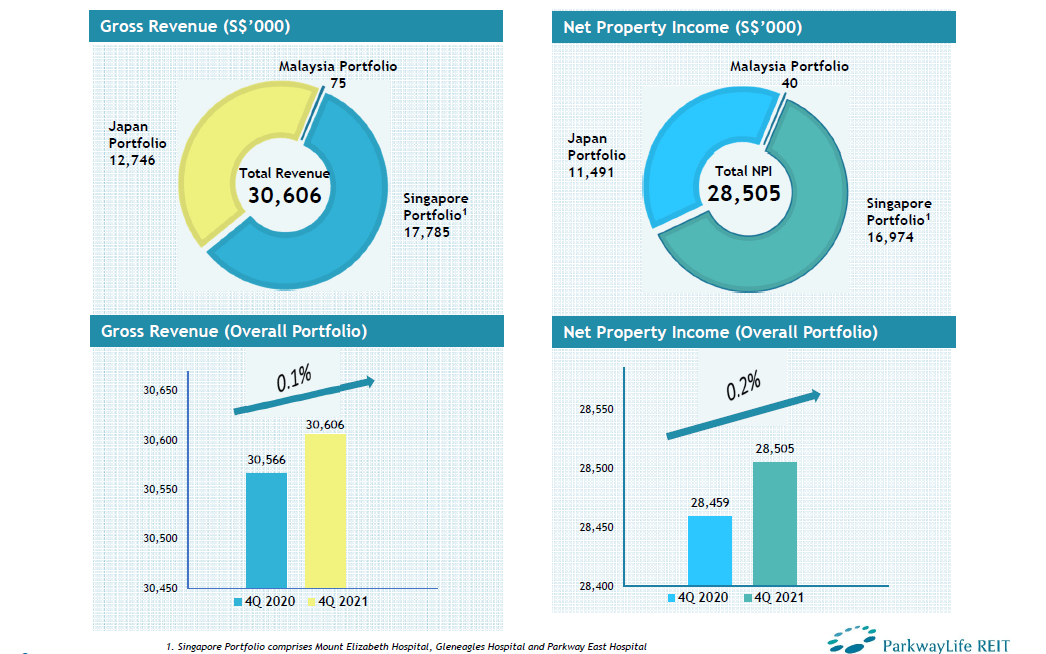

Parkway Life REIT has a portfolio of 52 Japan nursing care homes, the Mount Elizabeth, Gleneagles and Parkway East Hospitals in Singapore, and MOB Specialist Clinics in Malaysia.

As with any REIT, investors will want to focus on a sustainably rising dividend, or distribution per unit (DPU).

In Parkway Life REIT’s case, this rose 2.1% year-on-year in 2021 to 14.08 Singapore cents. However, for the fourth quarter of 2021, the DPU was flat year-on-year at 3.57 Singapore cents.

Meanwhile, gross revenue dipped 0.2% year-on-year for the whole of 2021 due to a divestment at the beginning of the year as well as weakness in the Japanese Yen (JPY).

On a quarterly basis, both gross revenue and net property income were up marginally (see below) across its 56 properties in the final three months of 2021.

Source: Parkway Life REIT Q4 2021 business update presentation

Robust debt and financing profile

In uncertain times like these, it helps to have a strong financial profile and Parkway Life REIT’s management continued to reaffirm that its capital position is extremely healthy.

Management revealed that it had put a JPY net income hedge in place until the second half of 2026 while it has also hedged its interest rate exposure.

Overall, as of the end of 2021, Parkway Life enjoys an unbelievably low all-in cost of debt of just 0.52%, perhaps a reflection of the easy monetary policy that’s ongoing in Japan.

Meanwhile, Parkway Life REIT’s gearing ratio is only 35.4% as of 31 December 2021 while its interest coverage ratio (ICR) is at 21.5x.

Change to semi-annual reporting

One thing dividend investors should take note of is that Parkway Life REIT announced that it is moving towards semi-annual financial reporting from this year.

As a result, the REIT will also align its dividend distributions with this timetable – paying out twice a year instead of its previous four times a year – and meaning Singapore’s market will have one less stock that pays out dividends every quarter.

Overall, it was another reliable quarter from the solid and defensive healthcare REIT. Given healthcare is generally perceived as “safe” in times of turbulence, investors just have to accept a lower dividend yield.

That’s certainly the case for Parkway Life REIT, with its 12-month forward distribution yield at 2.9% based on its latest unit price.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips owns shares of Parkway Life REIT.