The selling pressure in the US stock market continued into May as the S&P 500 Index and NASDAQ Composite Index were both down by 14.2% and 23.4% year-to-date, respectively.

It is a test of nerves for investors as the “easy money” era comes to an end.

That’s because the US Federal Reserve (Fed) continued with its monetary policy tightening path with a 50 basis points (bps) rate hike at the beginning of this month.

However, despite the end of the easy money era, I believe investors should buy into payments processing giant Visa Inc (NYSE: V) and take advantage of the market weakness to beef up their portfolio.

Visa was also featured in our 5 Top Stocks to Buy in May. Following on from that, here are five reasons why I think investors should buy Visa shares despite the of the easy monetary policy era.

1. Return of international travel fuels earnings

Visa has just reported a strong second-quarter earnings period for its financial year 2022 (Q2 FY2022), surpassing analysts’ average expectations.

It is impressive considering the loss of Russia’s revenue during the quarter.

The credit card company reported revenue of US$7.2 billion in Q2 FY2022, easily outpacing analysts’ average expectations of US$6.8 billion. It represents 25% growth as compared to a year ago.

In terms of earnings, Visa’s adjusted earnings per share (EPS) grew by 30% over the prior year’s EPS to US$1.79, beating analysts’ average expectations of US$1.65.

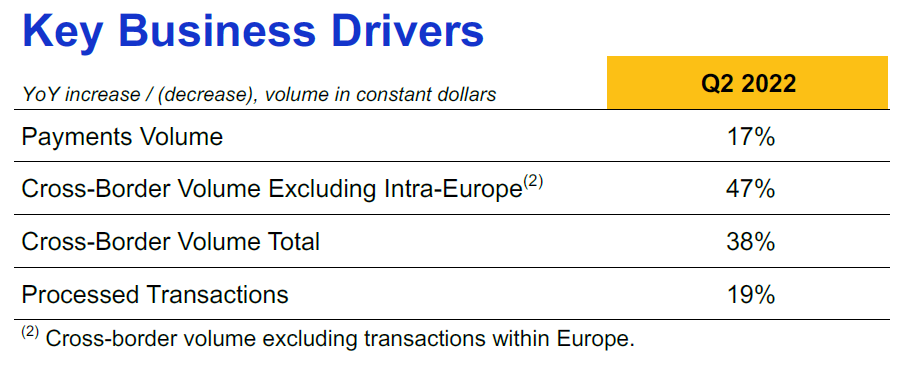

From the earnings results, what we saw is the return of travel demand. Higher travel has a positive impact on Visa as seen by the increase of 17% in payment volumes during the quarter.

Total cross-border volume was up by 38%, as total processed transactions grew by 19% compared to a year ago.

Source: VISA’s Q2 FY2022 Earnings Presentation

Source: VISA’s Q2 FY2022 Earnings Presentation

I think the earnings results in the Q2 FY2022 period supports the basis that Visa will be one of the major beneficiaries of the return of travel this year, especially during the year-end holidays.

2. Strong competitive advantage against peers

I was one of those who thought that the emergence of Big Tech players in the payments space will derail Visa’s competitive advantage.

However, it turns out that the strength of Visa’s network, that was built across the years among issuing banks and merchants, and the cost advantage and reputation of its secured payment network are very valuable.

For example, Apple Pay and Google Pay have both opted to enter the payments space by building their mobile payment platforms on top of the existing payment network infrastructure, such as Visa.

There were other efforts to reduce the reliance on Visa and Mastercard Inc (NYSE: MA), such as the European Payments Initiative aimed at creating a European payment network alternative.

However, the project was abandoned after most of the financial institutions working on the project decided to scrap it.

As seen in the past, the large investments, effort and time required to build a payments infrastructure network as big and reliable as Visa, will continue to be a deterrent to any new player.

3. Booming electronic payments will drive growth

Over the last decade, Visa has maintained a 10.6% compound annual growth rate (CAGR) in its revenue while EPS increased at 15.1% CAGR amid margin improvement and share buybacks.

In the US, electronic payments are already at a high penetration level of around 75% to 80% but the shift towards e-commerce and mobile will propel card payment usage higher.

Meanwhile, other regions around the world remain behind in terms of card payments. This offers booming growth opportunities ahead for Visa.

While Visa has a strong presence in the business-to-consumer (B2C) market, it is also moving into the business-to-business (B2B) market segment.

In the Group’s cross-border B2B business segment, Visa B2B Connect has expanded its global footprint by adding banks in Tanzania, Uganda, Angola, Thailand and Poland during the first half of 2022.

Visa also enables new ways to pay from installments to crypto. In the crypto space, Visa is working with governments globally on potential Central Bank Digital Currencies (CBDCs).

During the quarter, Visa was selected as the finalist in Brazil’s CBDC lift challenge.

4. Inflationary environment benefits Visa

Aside from generic growth, Visa is in a position to thrive from the inflationary environment.

About 70% of the Group’s revenue takes into account inflation as the fees charged are based on a percentage of total consumer spending.

Demand for Visa should also remain relatively resilient as it offers essential services to merchants and banks.

The high margin of Visa’s business is also another advantage.

As payment processing is a highly scalable business with most of the operating expenses fixed, the profitability of Visa should be less affected by the persistently high inflation environment.

5. Fairly priced with dividend safety

Currently, Visa is trading at a PE ratio of 29.5 times, which is less than its five-year average PE of 35.7 times.

Given the potential coming from the return of international travel, I am optimistic that the valuation is fairly priced and could see even see upside potential.

There are other moving parts, especially the fluctuation of foreign exchange (FX) as well as the impact from the Russia-Ukraine war.

However, given its fair valuation and a dividend yield of 0.7%, I think Visa is a good stock for long-term investors to accumulate.

While its dividend yield is low, its dividend payout ratio is only 21% and the dividend per share (DPS) has been growing over the last 13 years.

Visa offers stability in the near term

It is hard to pick the right stock amid a sea of red. When investors are in panic mode, it is easy to make emotional decisions.

My colleague, Tim, has just written an interesting piece on 3 Smart Warren Buffett Quotes to Remember Amid the Current Market Crash.

I think Visa will suit investors who can’t stomach the big drops seen in some of the Big Tech companies in the near term and should offer the stability for investors.

If you are looking for a company that thrives on the return of international travel and amid an inflationary environment, you should buy Visa’s shares even though the end of the easy money era could depress some of the valuations of listed stocks.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.