I don’t usually comment on companies that I think are not worth buying, in part because I believe that the value of a stock needs to be viewed from the objective of an individual.

Having said that, I think it is important to address one of the big talking points of recent days.:

I’m, of course, referring to Elon Musk’s acquisition of 9.2% in Twitter Inc (NYSE: TWTR), which subsequently led to a surge in the struggling social media firm’s share price.

With the acquisition, Musk now appears to be the largest shareholder, overtaking Twitter’s founder and former CEO, Jack Dorsey.

However, it is unclear what Musk has in mind for Twitter but the world’s richest man has been vocal in his criticism of the company’s failure to adhere to free speech principles.

Despite the surge in the share price of Twitter following the news, I still think it’s too early to buy into Twitter.

In fact, I think the fundamentals of the company remain unchanged at this point of time. Here are three key reasons why I think Twitter is still not worth buying for long-term investors.

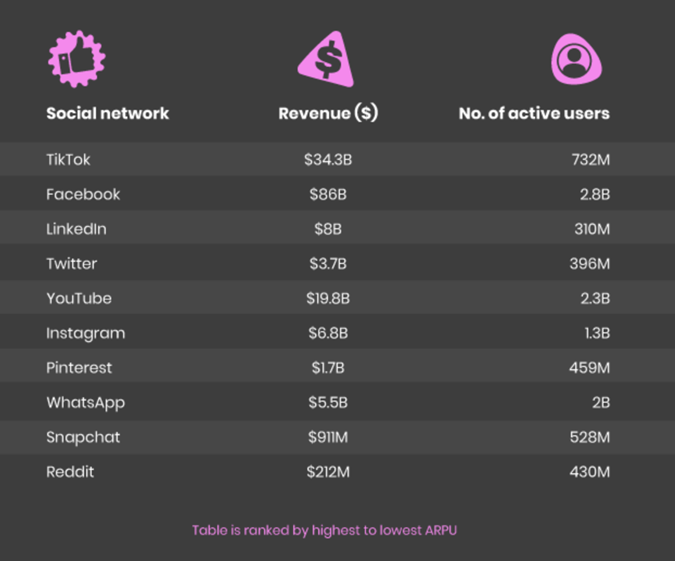

1. Twitter poor at generating revenue

One of the biggest problems with Twitter is the struggles it has to generate revenue as compared to its peers.

Despite its large user base and the importance of its social media platform, Twitter’s average revenue per user (ARPU) remains lower than its peers, such as Meta Platforms Inc (NASDAQ: FB).

Twitter ranked behind the likes of TikTok, Facebook and LinkedIn when it comes to ARPU.

Source: Postbeyond.com

Source: Postbeyond.com

2. Twitter gaining users but earnings fall

The good thing about Twitter is that it has managed to maintain steady monetisable daily active users (mDAUs), which rose 13% year-on-year to 217 million in the 4Q FY2021.

Its revenue also grew by 21% year-on-year during the same period.

However, Twitter’s adjusted earnings before interest, taxes, depreciation and amortization (EBITDA) saw a decline of 32% to US$628 million in 2021.

This is mainly due to increase in headcount by about 30% during the year. Twitter plans to boost its headcount by another 20% in 2022 with a focus on research & development (R&D).

3. Too many products not creating revenue

While I like some of the new product launches by Twitter, which include the short-lived “Fleets”, “topics” for tweets and even Twitter Blue subscriptions, none of them have manage to serve as an earnings lever for the company.

With a change of management in November last year, I think it will be even harder for Twitter’s new CEO, Parag Agrawal, to drive meaningful changes for the company in the near term.

In fact, the latest financial results also show that total ads engagement was down by 12%.

What will change my mind about Twitter?

At the moment, Musk is taking the status as a passive investor based on his 13G filing, indicating that he has no interest to pursue control of the company.

I believe if Musk were to take on a more active role, things might be a bit more different. Given Musk’s track record as an entrepreneur, I’ll keep an eye on the development on this front.

At this point, I still don’t see a compelling reason to buy Twitter and investors who are keen on the social media space would be better off investing in Meta.

For any current shareholders, I think it would make better sense for them to sell on the rally from the recent hype.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.